Welcome to the

2023 AI Index Report

The AI Index is an independent initiative at the Stanford Institute for Human-Centered Artificial Intelligence (HAI), led by the AI Index Steering Committee, an interdisciplinary group of experts from across academia and industry. The annual report tracks, collates, distills, and visualizes data relating to artificial intelligence, enabling decision-makers to take meaningful action to advance AI responsibly and ethically with humans in mind.

The AI Index collaborates with many different organizations to track progress in artificial intelligence. These organizations include: the Center for Security and Emerging Technology at Georgetown University, LinkedIn, NetBase Quid, Lightcast, and McKinsey. The 2023 report also features more self-collected data and original analysis than ever before. This year’s report included new analysis on foundation models, including their geopolitics and training costs, the environmental impact of AI systems, K-12 AI education, and public opinion trends in AI. The AI Index also broadened its tracking of global AI legislation from 25 countries in 2022 to 127 in 2023.

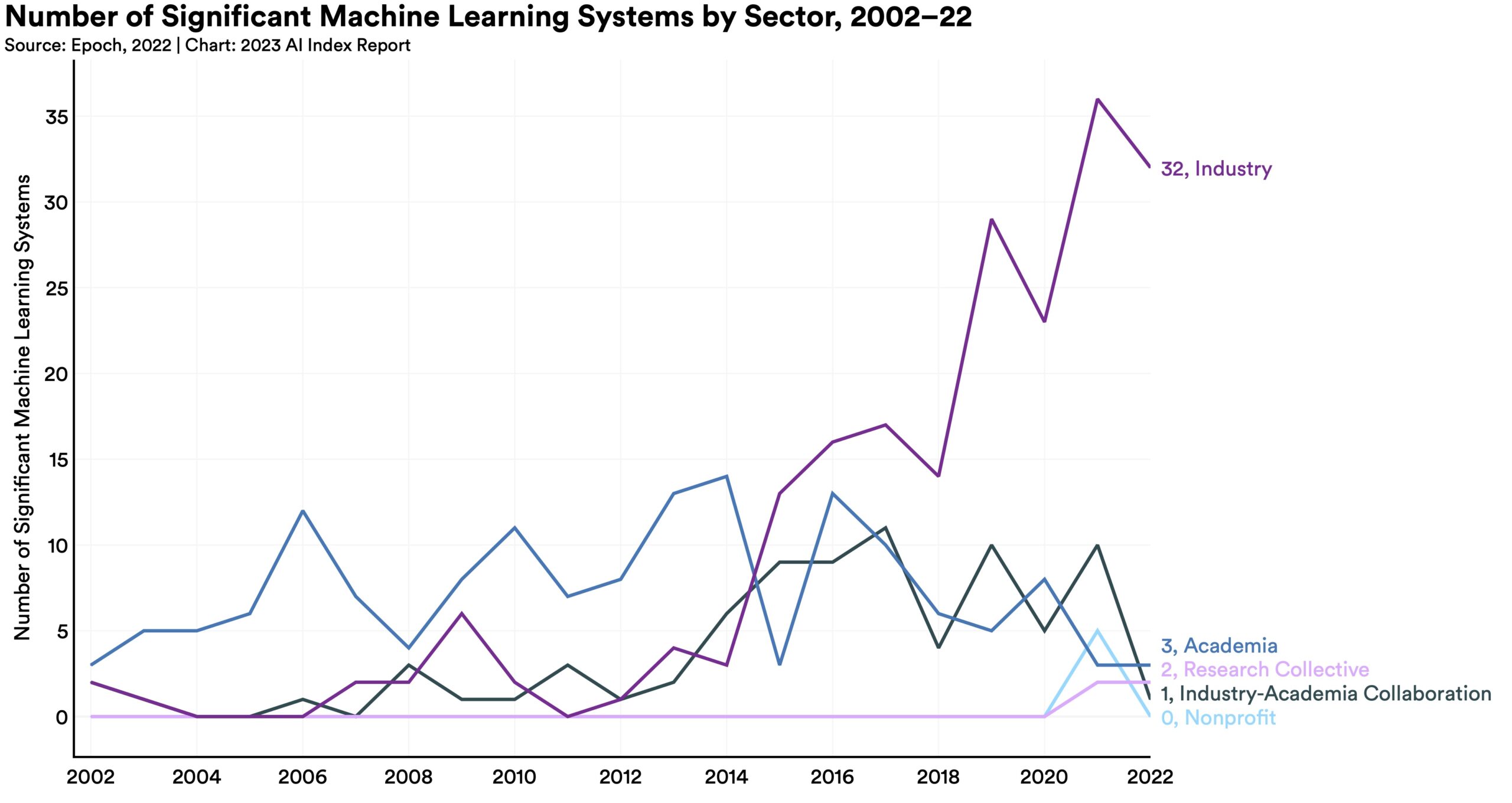

Until 2014, most significant machine learning models were released by academia. Since then, industry has taken over. In 2022, there were 32 significant industry-produced machine learning models compared to just three produced by academia. Building state-of-the-art AI systems increasingly requires large amounts of data, compute, and money, resources that industry actors inherently possess in greater amounts compared to nonprofits and academia.

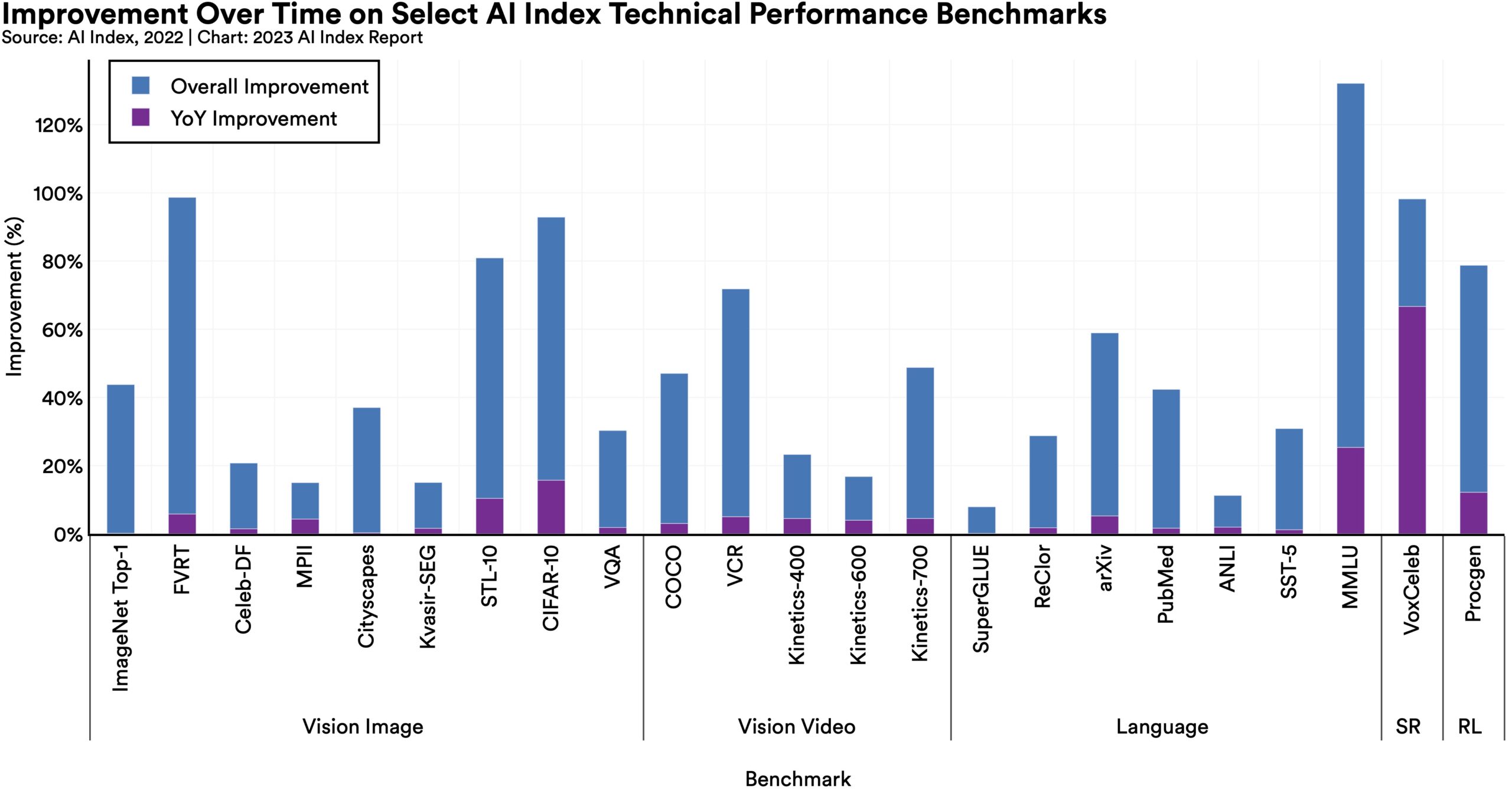

AI continued to post state-of-the-art results, but year-over-year improvement on many benchmarks continues to be marginal. Moreover, the speed at which benchmark saturation is being reached is increasing. However, new, more comprehensive benchmarking suites such as BIG-bench and HELM are being released.

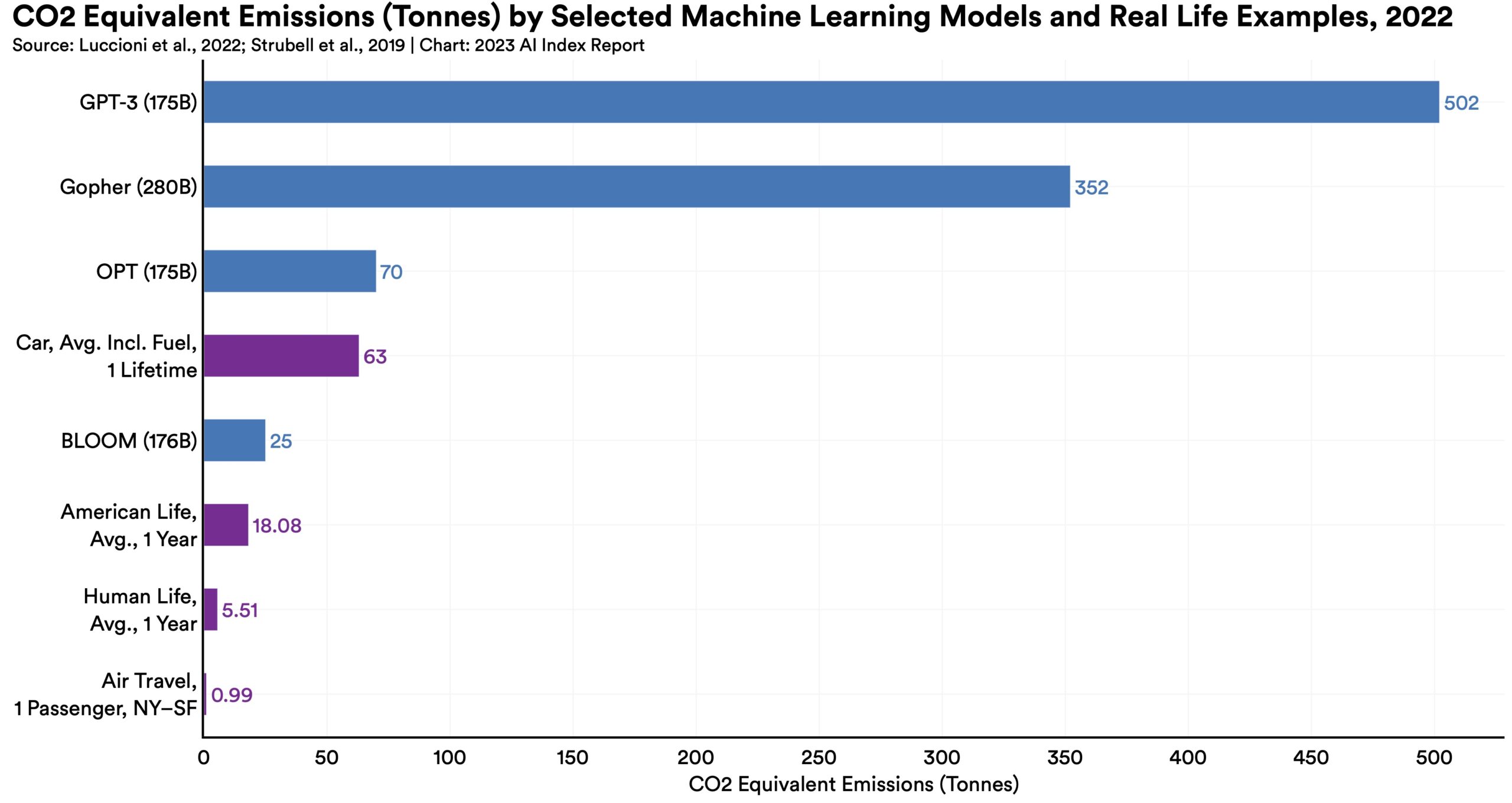

New research suggests that AI systems can have serious environmental impacts. According to Luccioni et al., 2022, BLOOM’s training run emitted 25 times more carbon than a single air traveler on a one-way trip from New York to San Francisco. Still, new reinforcement learning models like BCOOLER show that AI systems can be used to optimize energy usage.

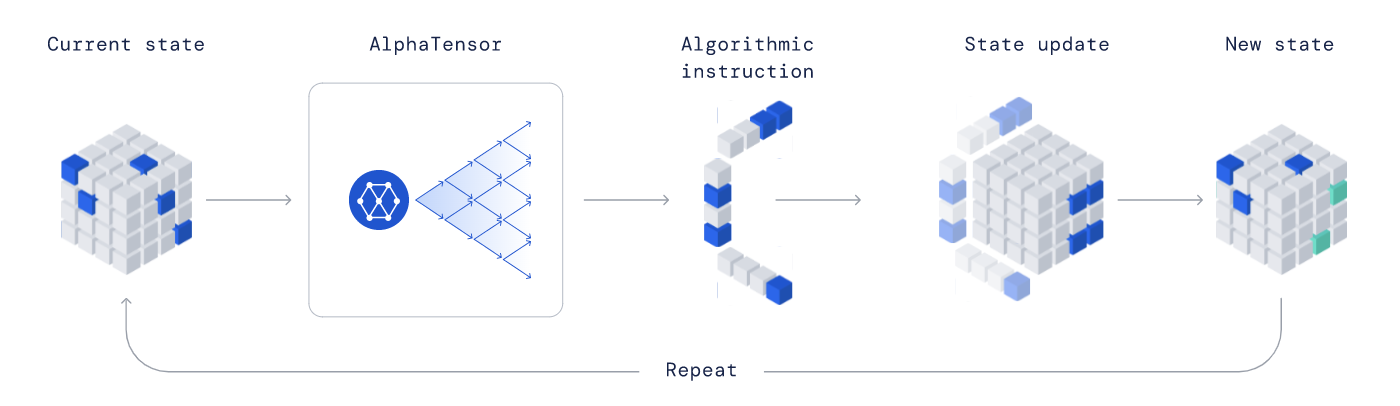

AI models are starting to rapidly accelerate scientific progress and in 2022 were used to aid hydrogen fusion, improve the efficiency of matrix manipulation, and generate new antibodies.

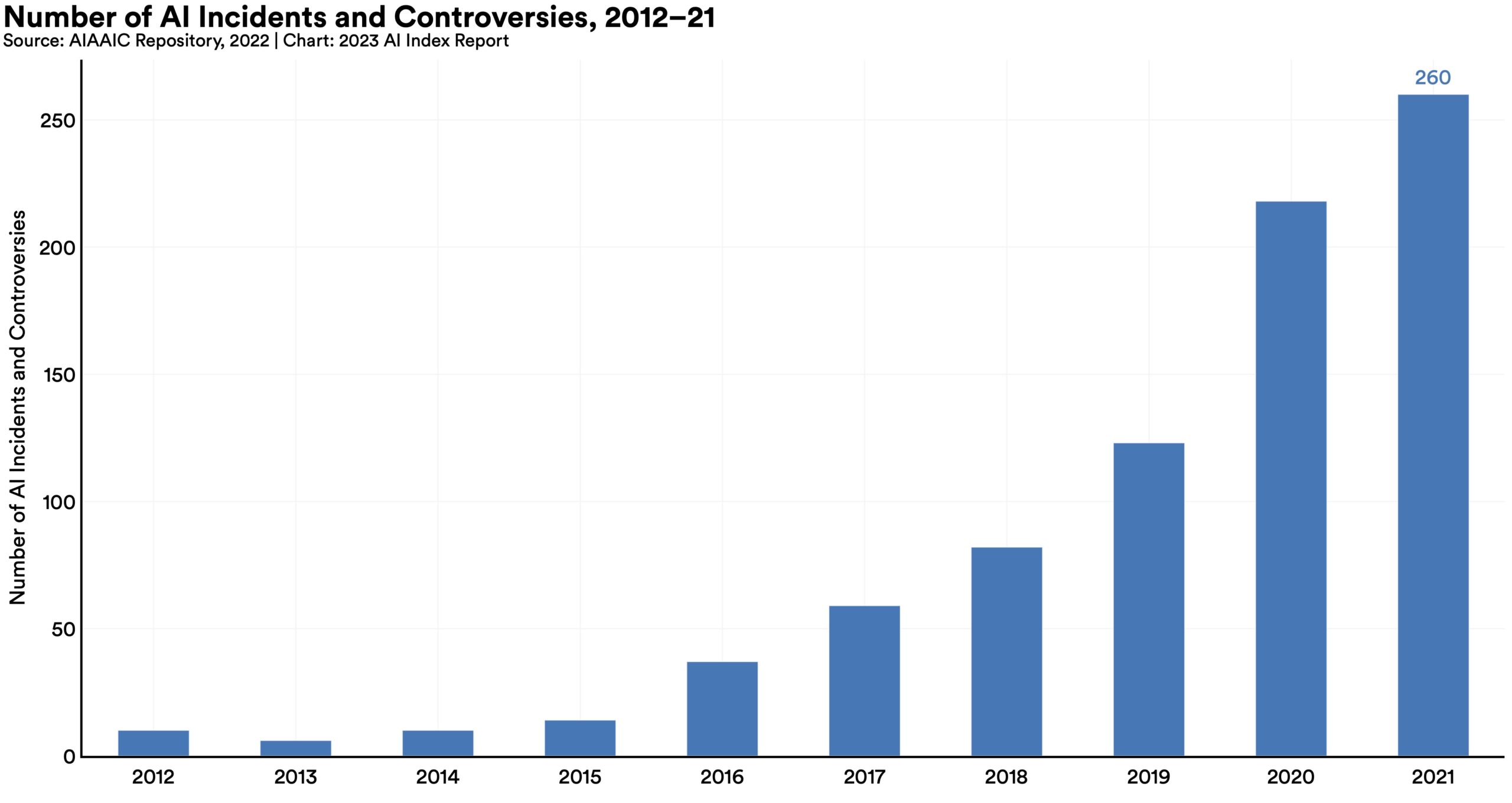

According to the AIAAIC database, which tracks incidents related to the ethical misuse of AI, the number of AI incidents and controversies has increased 26 times since 2012. Some notable incidents in 2022 included a deepfake video of Ukrainian President Volodymyr Zelenskyy surrendering and U.S. prisons using call-monitoring technology on their inmates. This growth is evidence of both greater use of AI technologies and awareness of misuse possibilities.

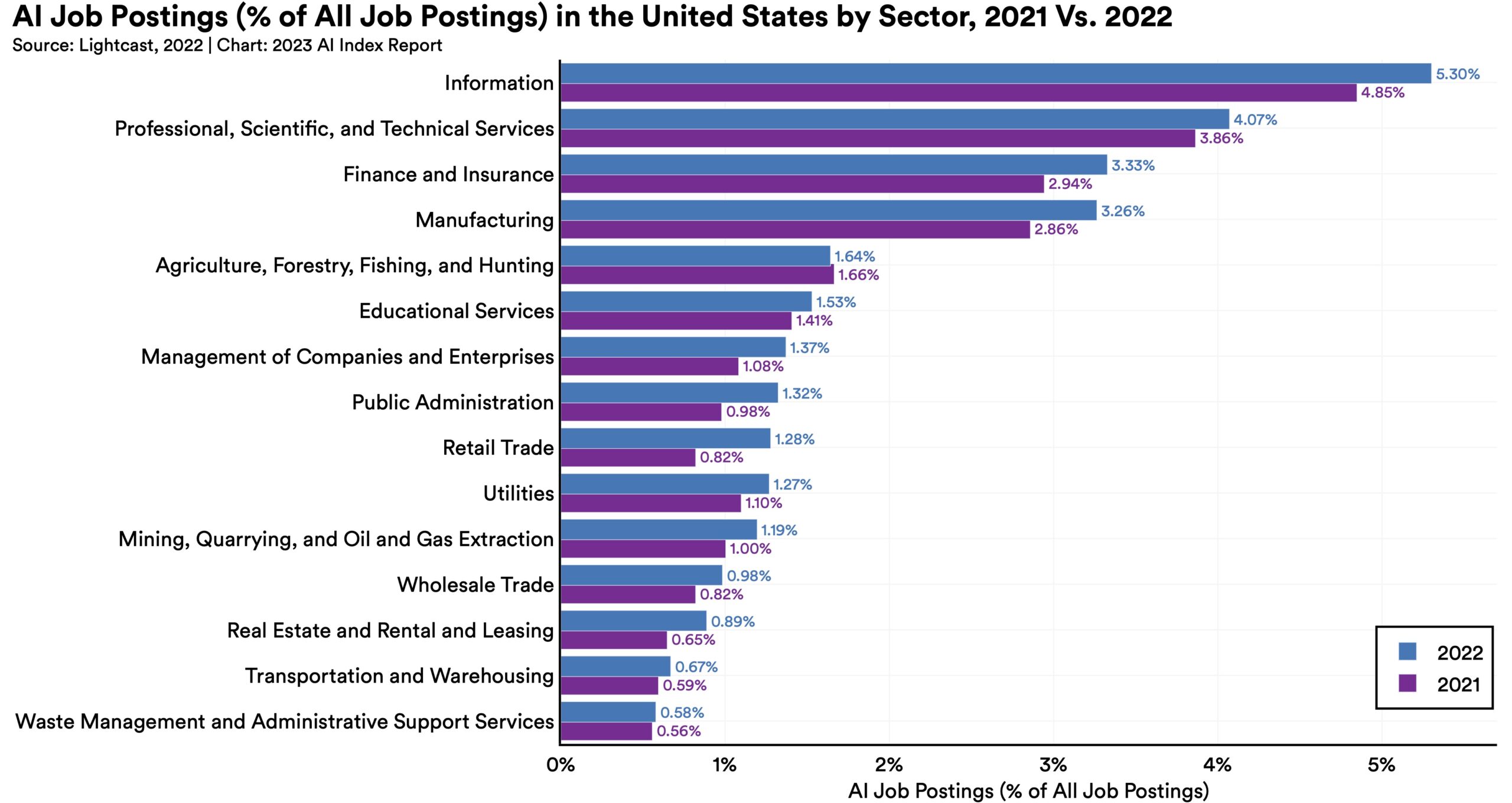

Across every sector in the United States for which there is data (with the exception of agriculture, forestry, fishery and hunting), the number of AI-related job postings has increased on average from 1.7% in 2021 to 1.9% in 2022. Employers in the United States are increasingly looking for workers with AI-related skills.

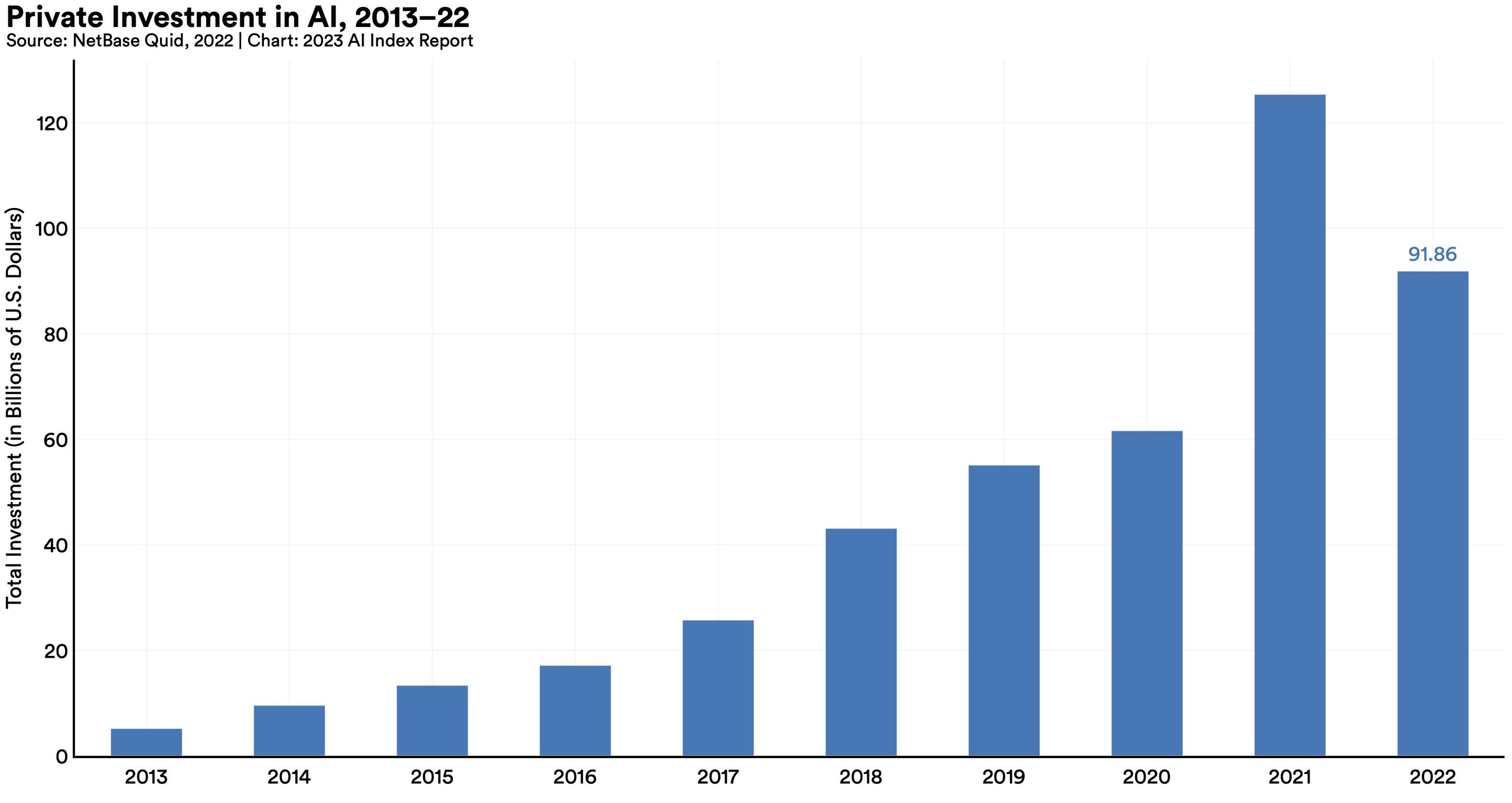

Global AI private investment was $91.9 billion in 2022, which represented a 26.7% decrease since 2021. The total number of AI-related funding events as well as the number of newly funded AI companies likewise decreased. Still, during the last decade as a whole, AI investment has significantly increased. In 2022 the amount of private investment in AI was 18 times greater than it was in 2013.

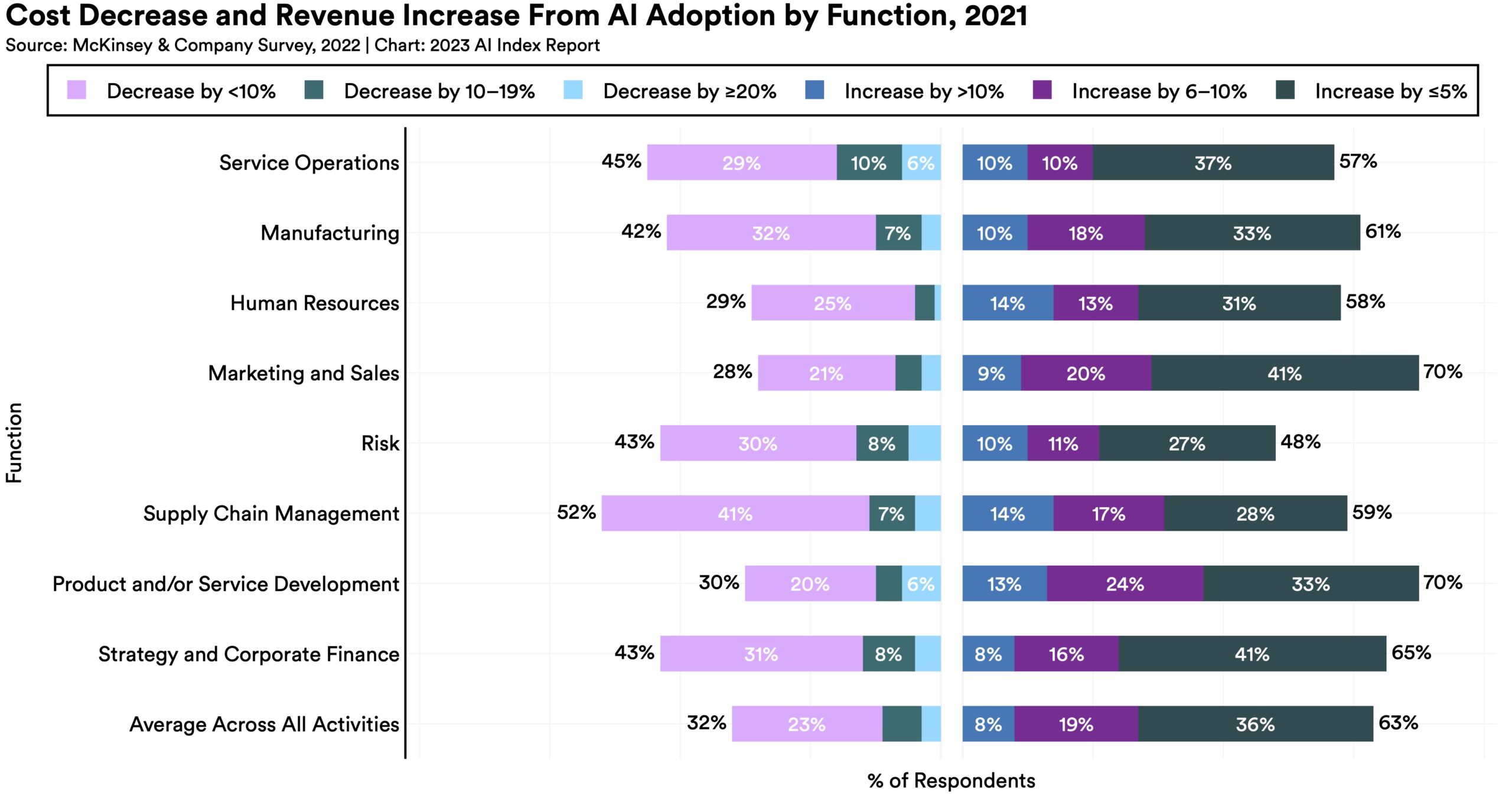

The proportion of companies adopting AI in 2022 has more than doubled since 2017, though it has plateaued in recent years between 50% and 60%, according to the results of McKinsey’s annual research survey. Organizations that have adopted AI report realizing meaningful cost decreases and revenue increases.

An AI Index analysis of the legislative records of 127 countries shows that the number of bills containing “artificial intelligence” that were passed into law grew from just 1 in 2016 to 37 in 2022. An analysis of the parliamentary records on AI in 81 countries likewise shows that mentions of AI in global legislative proceedings have increased nearly 6.5 times since 2016.

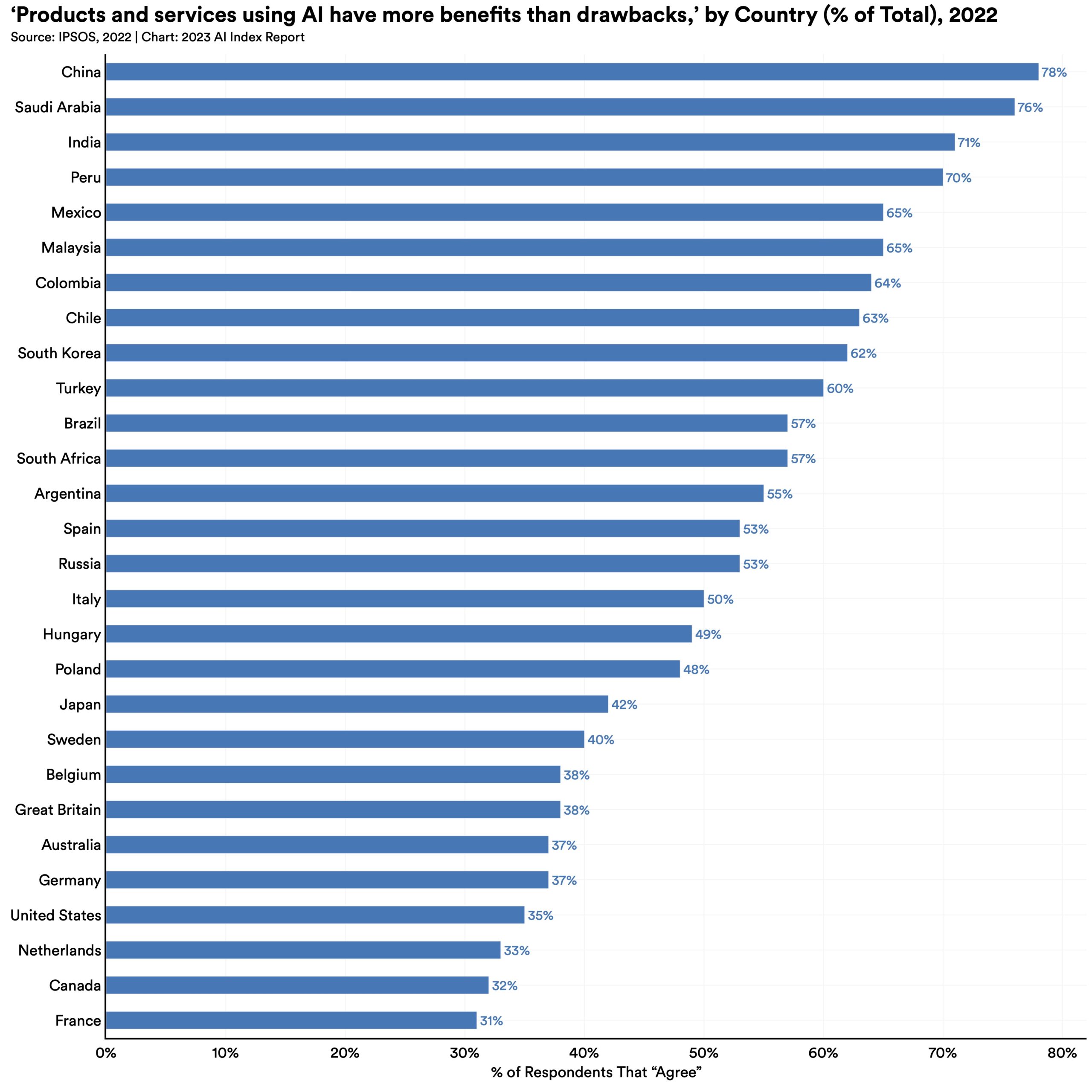

In a 2022 IPSOS survey, 78% of Chinese respondents (the highest proportion of surveyed countries) agreed with the statement that products and services using AI have more benefits than drawbacks. After Chinese respondents, those from Saudi Arabia (76%) and India (71%) felt the most positive about AI products. Only 35% of sampled Americans (among the lowest of surveyed countries) agreed that products and services using AI had more benefits than drawbacks.

This chapter captures trends in AI R&D. It begins by examining AI publications, including journal articles, conference papers, and repositories. Next it considers data on significant machine learning systems, including large language and multimodal models. Finally, the chapter concludes by looking at AI conference attendance and open-source AI research. Although the United States and China continue to dominate AI R&D, research efforts are becoming increasingly geographically dispersed.

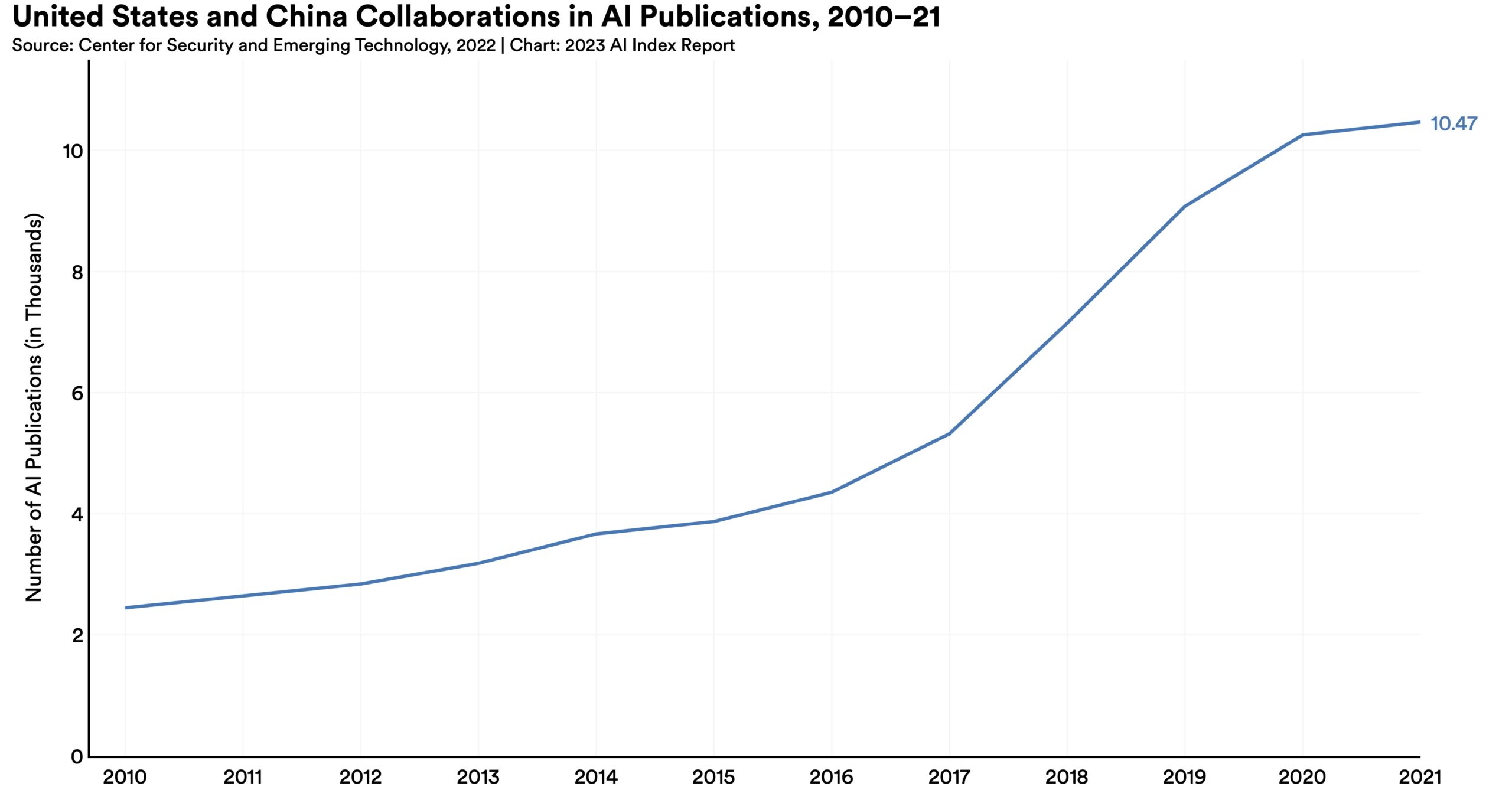

The number of AI research collaborations between the United States and China increased roughly 4 times since 2010, and was 2.5 times greater than the collaboration totals of the next nearest country pair, the United Kingdom and China. However, the total number of U.S.-China collaborations only increased by 2.1% from 2020 to 2021, the smallest year-over-year growth rate since 2010.

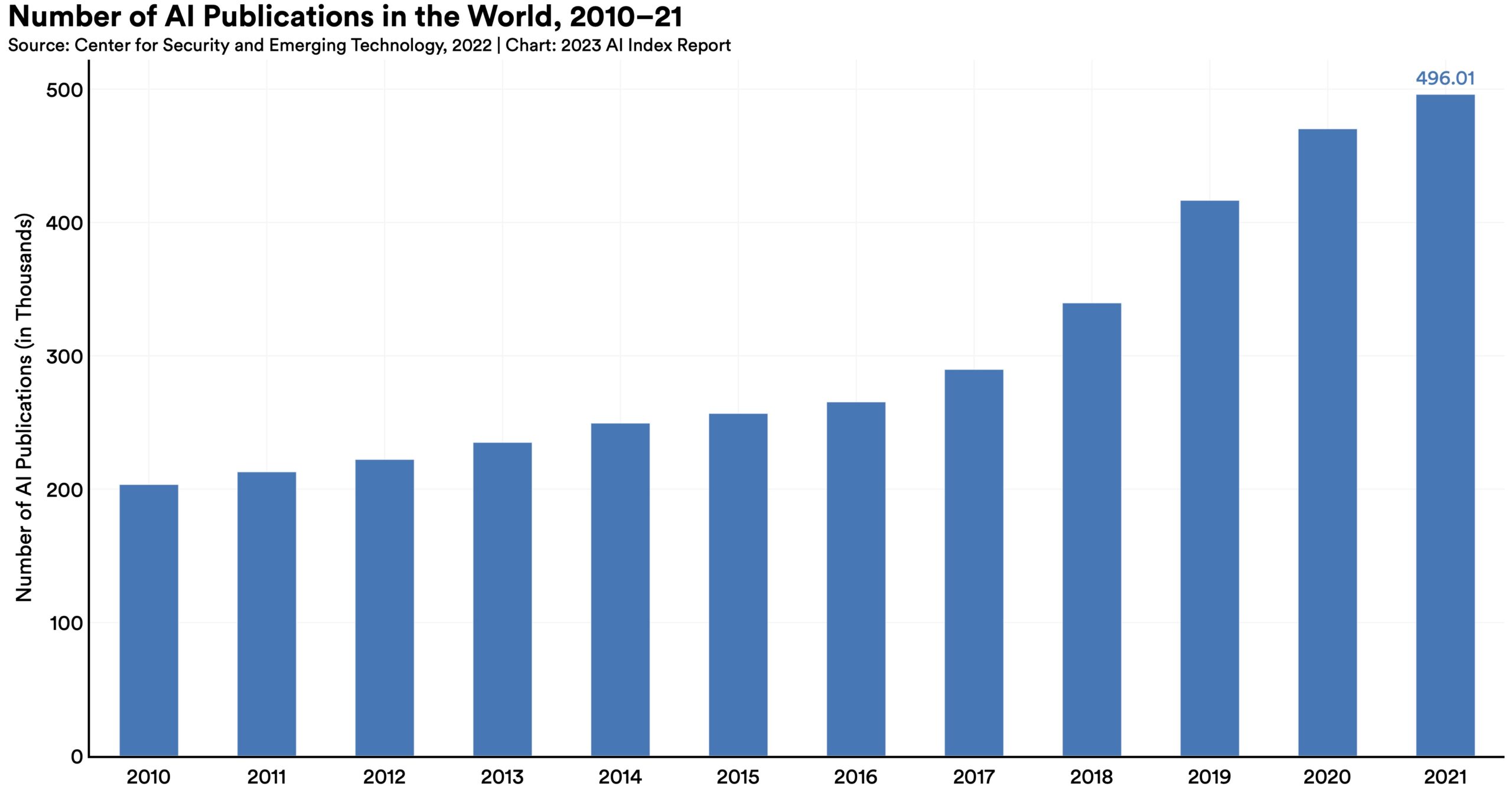

The number of AI research collaborations between the United States and China increased roughly 4 times since 2010, and was 2.5 times greater than the collaboration totals of the next nearest country pair, the United Kingdom and China. However, the total number of U.S.-China collaborations only increased by 2.1% from 2020 to 2021, the smallest year-over-year growth rate since 2010.  The total number of AI publications has more than doubled since 2010. The specific AI topics that continue to dominate research include pattern recognition, machine learning, and computer vision.

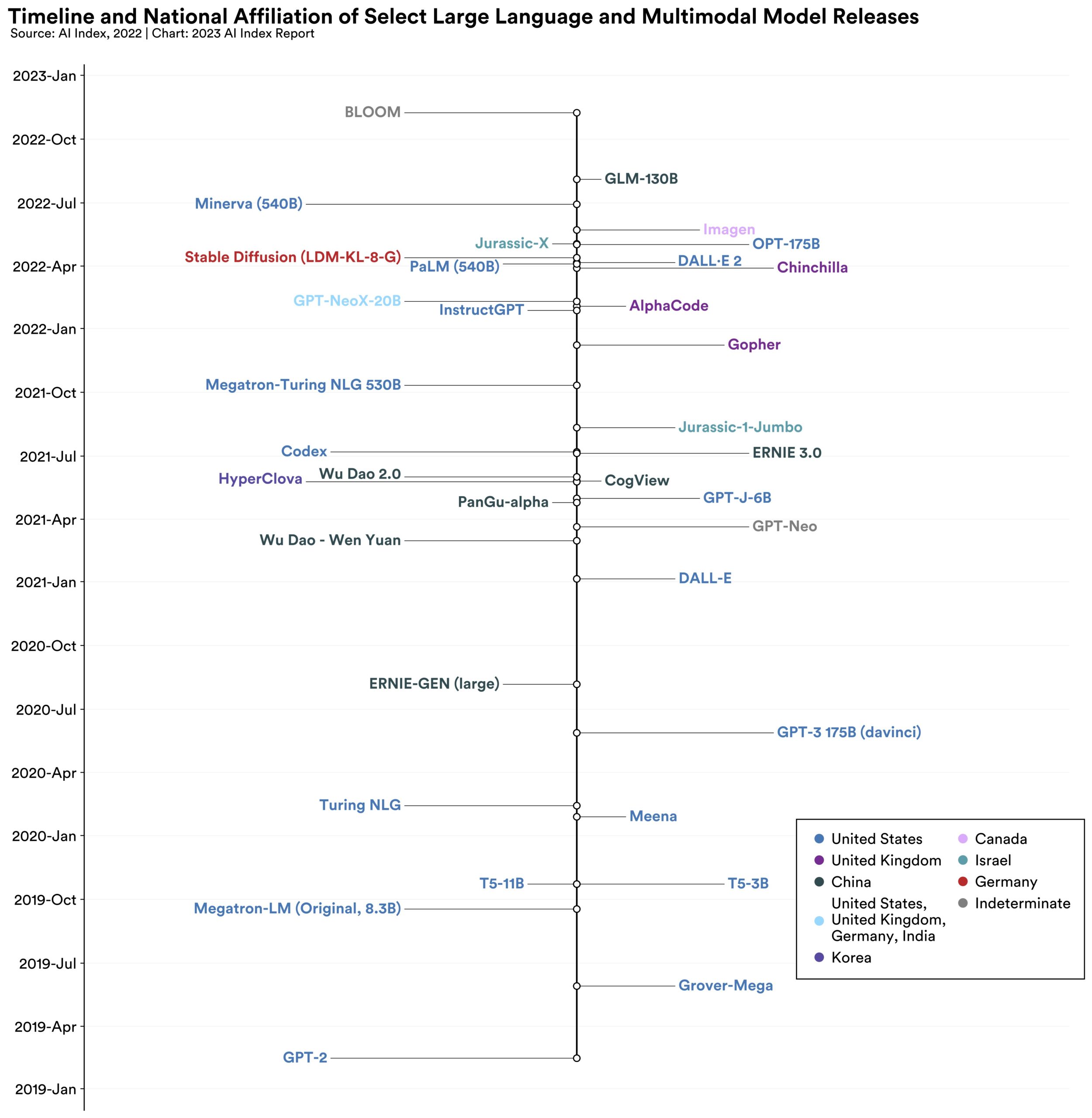

The total number of AI publications has more than doubled since 2010. The specific AI topics that continue to dominate research include pattern recognition, machine learning, and computer vision.  The United States is still ahead in terms of AI conference and repository citations, but those leads are slowly eroding. Still, the majority of the world’s large language and multimodal models (54% in 2022) are produced by American institutions.

The United States is still ahead in terms of AI conference and repository citations, but those leads are slowly eroding. Still, the majority of the world’s large language and multimodal models (54% in 2022) are produced by American institutions.  Until 2014, most significant machine learning models were released by academia. Since then, industry has taken over. In 2022, there were 32 significant industry-produced machine learning models compared to just three produced by academia. Building state-of-the-art AI systems increasingly requires large amounts of data, computer power, and money—resources that industry actors inherently possess in greater amounts compared to nonprofits and academia.

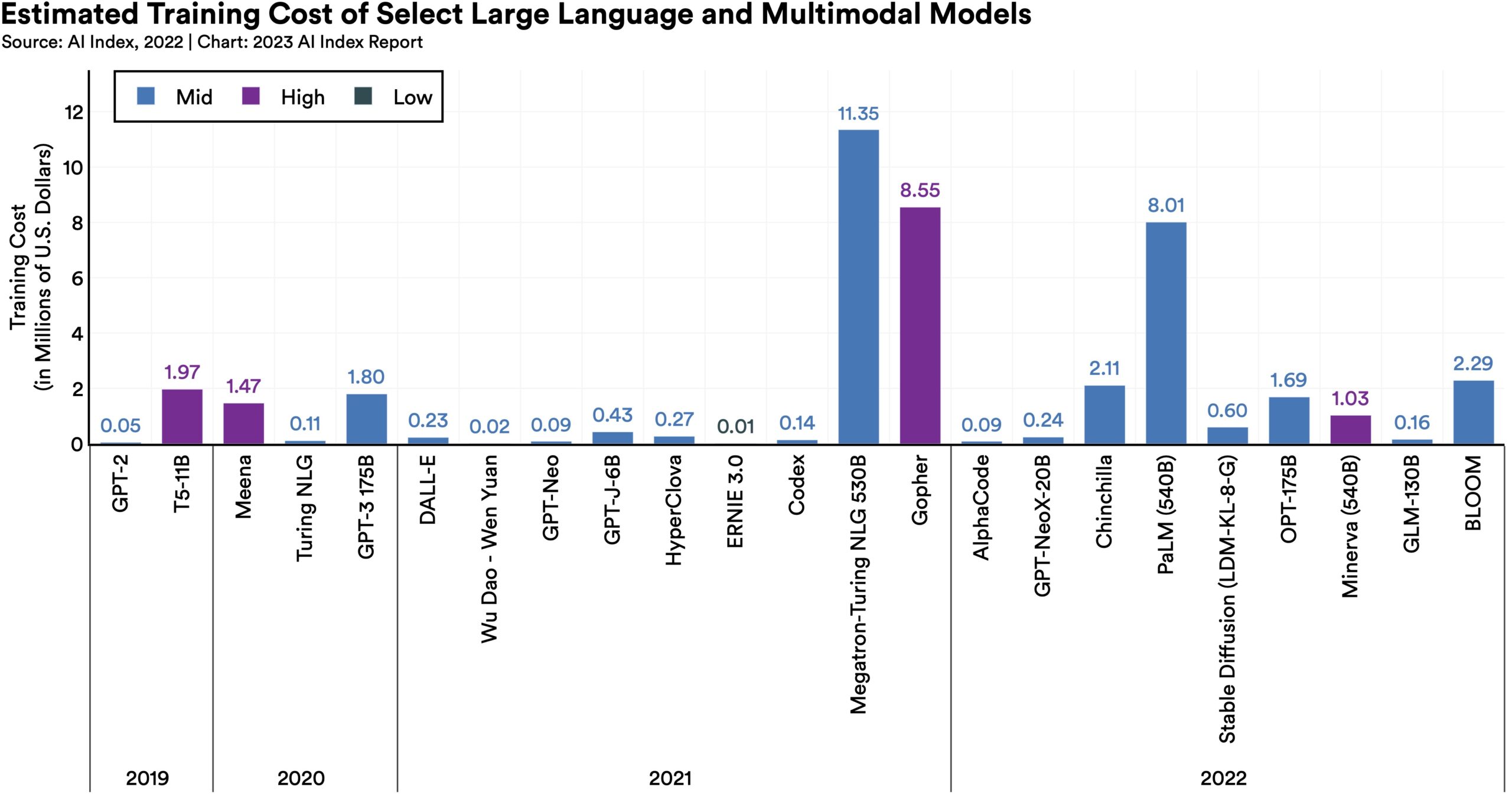

Until 2014, most significant machine learning models were released by academia. Since then, industry has taken over. In 2022, there were 32 significant industry-produced machine learning models compared to just three produced by academia. Building state-of-the-art AI systems increasingly requires large amounts of data, computer power, and money—resources that industry actors inherently possess in greater amounts compared to nonprofits and academia.  GPT-2, released in 2019, considered by many to be the first large language model, had 1.5 billion parameters and cost an estimated $50,000 USD to train. PaLM, one of the flagship large language models launched in 2022, had 540 billion parameters and cost an estimated $8 million USD—PaLM was around 360 times larger than GPT-2 and cost 160 times more. It’s not just PaLM: Across the board, large language and multimodal models are becoming larger and pricier.

GPT-2, released in 2019, considered by many to be the first large language model, had 1.5 billion parameters and cost an estimated $50,000 USD to train. PaLM, one of the flagship large language models launched in 2022, had 540 billion parameters and cost an estimated $8 million USD—PaLM was around 360 times larger than GPT-2 and cost 160 times more. It’s not just PaLM: Across the board, large language and multimodal models are becoming larger and pricier. This year’s technical performance chapter features analysis of the technical progress in AI during 2022. Building on previous reports, this chapter chronicles advancement in computer vision, language, speech, reinforcement learning, and hardware. Moreover, this year this chapter features an analysis on the environmental impact of AI, a discussion of the ways in which AI has furthered scientific progress, and a timeline-style overview of some of the most significant recent AI developments.

AI continued to post state-of-the-art results, but year-over-year improvement on many benchmarks continues to be marginal. Moreover, the speed at which benchmark saturation is being reached is increasing. However, new, more comprehensive benchmarking suites such as BIG-bench and HELM are being released.

AI continued to post state-of-the-art results, but year-over-year improvement on many benchmarks continues to be marginal. Moreover, the speed at which benchmark saturation is being reached is increasing. However, new, more comprehensive benchmarking suites such as BIG-bench and HELM are being released.  2022 saw the release of text-to-image models like DALL-E 2 and Stable Diffusion, text-to-video systems like Make-A-Video, and chatbots like ChatGPT. Still, these systems can be prone to hallucination, confidently outputting incoherent or untrue responses, making it hard to rely on them for critical applications.

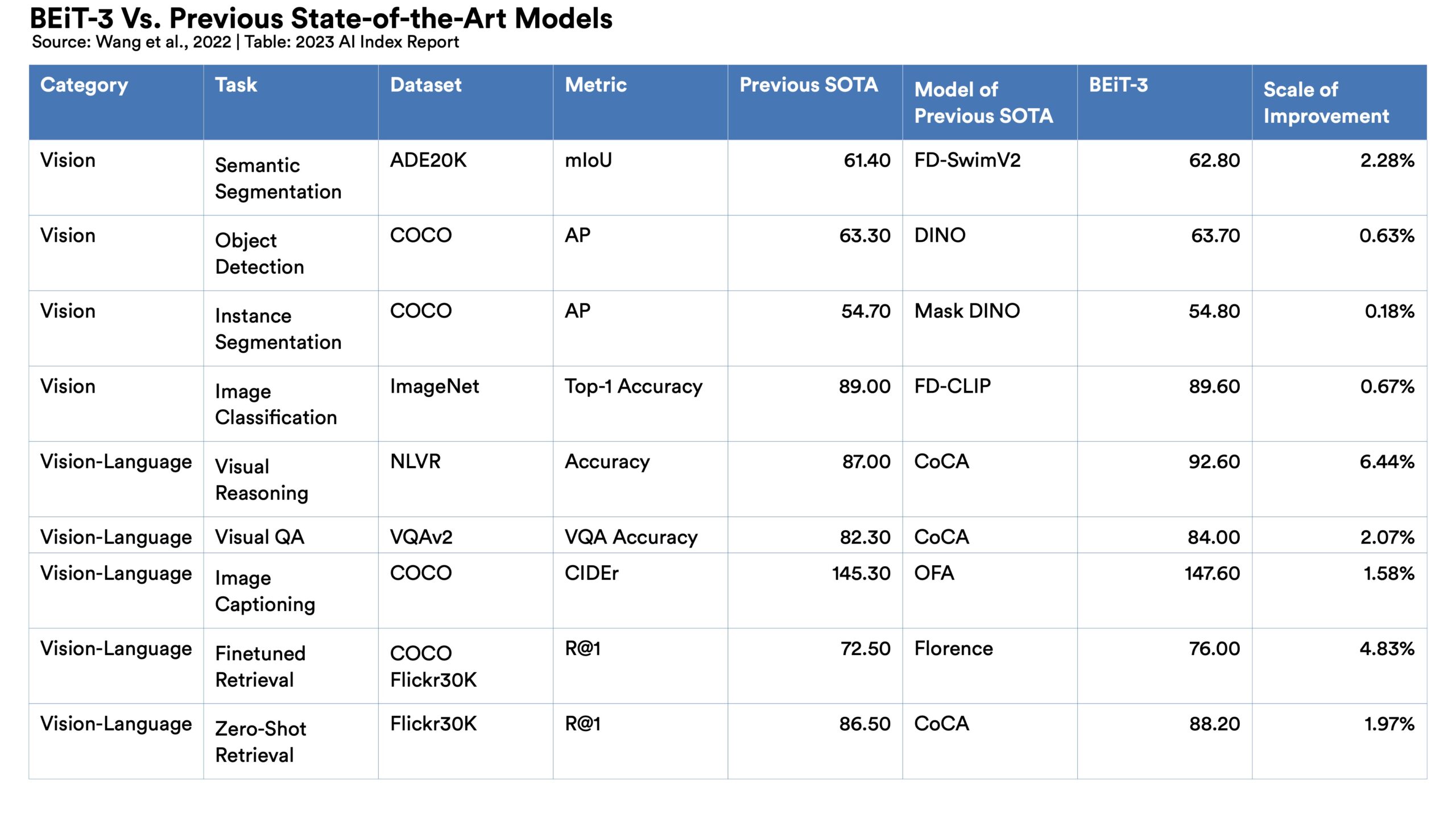

2022 saw the release of text-to-image models like DALL-E 2 and Stable Diffusion, text-to-video systems like Make-A-Video, and chatbots like ChatGPT. Still, these systems can be prone to hallucination, confidently outputting incoherent or untrue responses, making it hard to rely on them for critical applications.  Traditionally AI systems have performed well on narrow tasks but have struggled across broader tasks. Recently released models challenge that trend; BEiT-3, PaLI, and Gato, among others, are single AI systems increasingly capable of navigating multiple tasks (for example, vision, language).

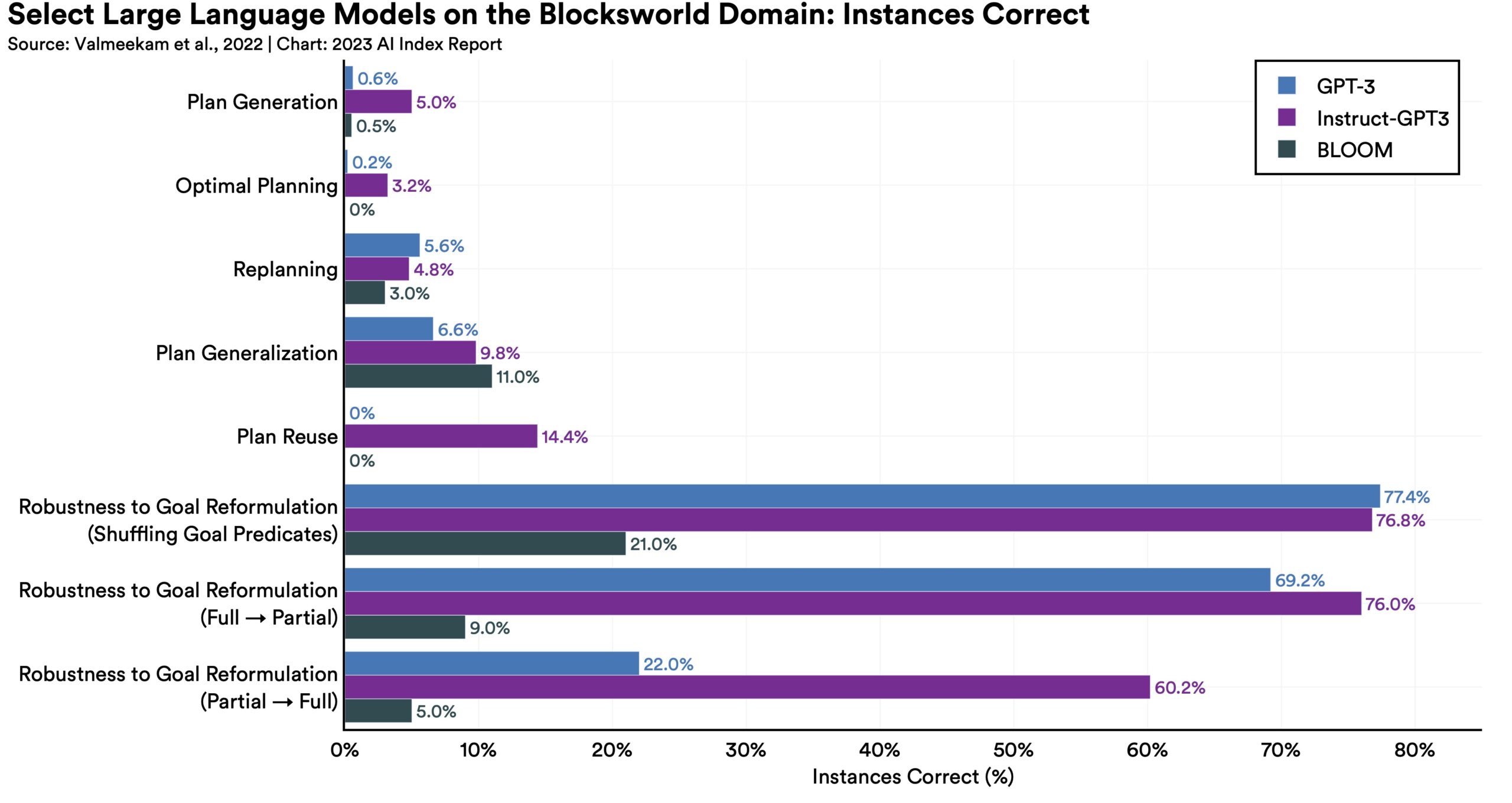

Traditionally AI systems have performed well on narrow tasks but have struggled across broader tasks. Recently released models challenge that trend; BEiT-3, PaLI, and Gato, among others, are single AI systems increasingly capable of navigating multiple tasks (for example, vision, language).  Language models continued to improve their generative capabilities, but new research suggests that they still struggle with complex planning tasks.

Language models continued to improve their generative capabilities, but new research suggests that they still struggle with complex planning tasks.

New research suggests that AI systems can have serious environmental impacts. According to Luccioni et al., 2022, BLOOM’s training run emitted 25 times more carbon than a single air traveler on a one-way trip from New York to San Francisco. Still, new reinforcement learning models like BCOOLER show that AI systems can be used to optimize energy usage.

New research suggests that AI systems can have serious environmental impacts. According to Luccioni et al., 2022, BLOOM’s training run emitted 25 times more carbon than a single air traveler on a one-way trip from New York to San Francisco. Still, new reinforcement learning models like BCOOLER show that AI systems can be used to optimize energy usage.  AI models are starting to rapidly accelerate scientific progress and in 2022 were used to aid hydrogen fusion, improve the efficiency of matrix manipulation, and generate new antibodies.

AI models are starting to rapidly accelerate scientific progress and in 2022 were used to aid hydrogen fusion, improve the efficiency of matrix manipulation, and generate new antibodies.

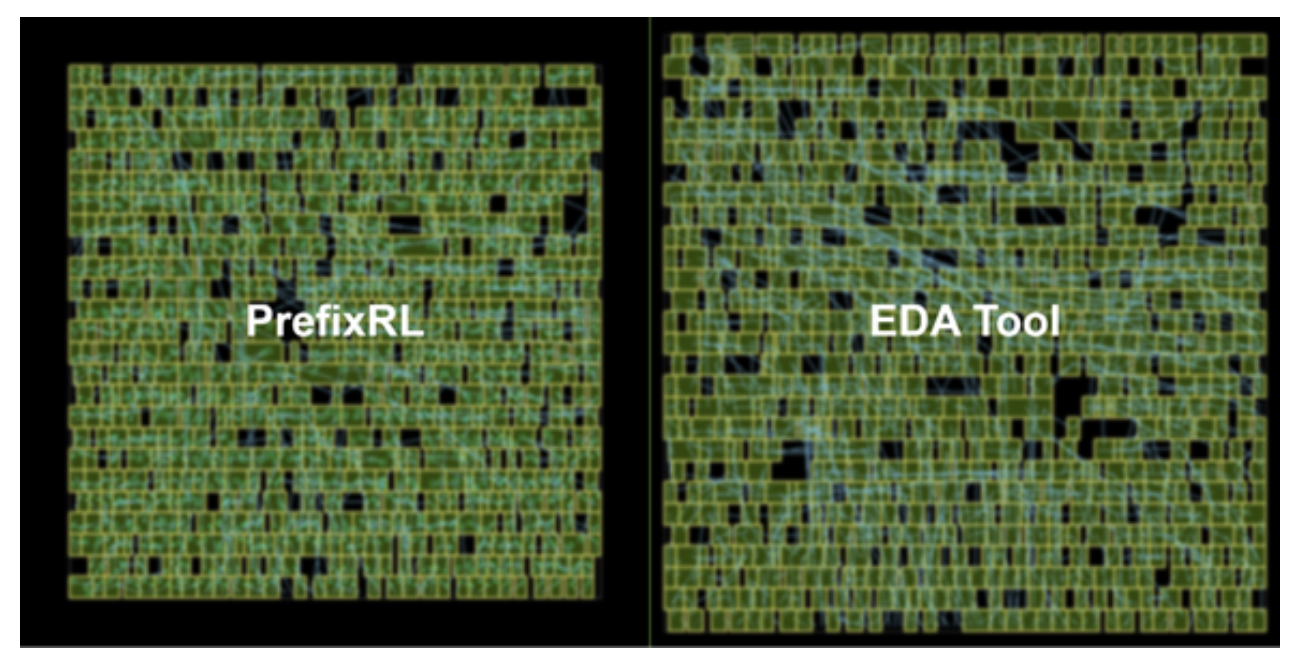

Nvidia used an AI reinforcement learning agent to improve the design of the chips that power AI systems. Similarly, Google recently used one of its language models, PaLM, to suggest ways to improve the very same model. Self-improving AI learning will accelerate AI progress.

Nvidia used an AI reinforcement learning agent to improve the design of the chips that power AI systems. Similarly, Google recently used one of its language models, PaLM, to suggest ways to improve the very same model. Self-improving AI learning will accelerate AI progress. Fairness, bias, and ethics in machine learning continue to be topics of interest among both researchers and practitioners. As the technical barrier to entry for creating and deploying generative AI systems has lowered dramatically, the ethical issues around AI have become more apparent to the general public. Startups and large companies find themselves in a race to deploy and release generative models, and the technology is no longer controlled by a small group of actors.

In addition to building on analysis in last year’s report, this year the AI Index highlights tensions between raw model performance and ethical issues, as well as new metrics quantifying bias in multimodal models.

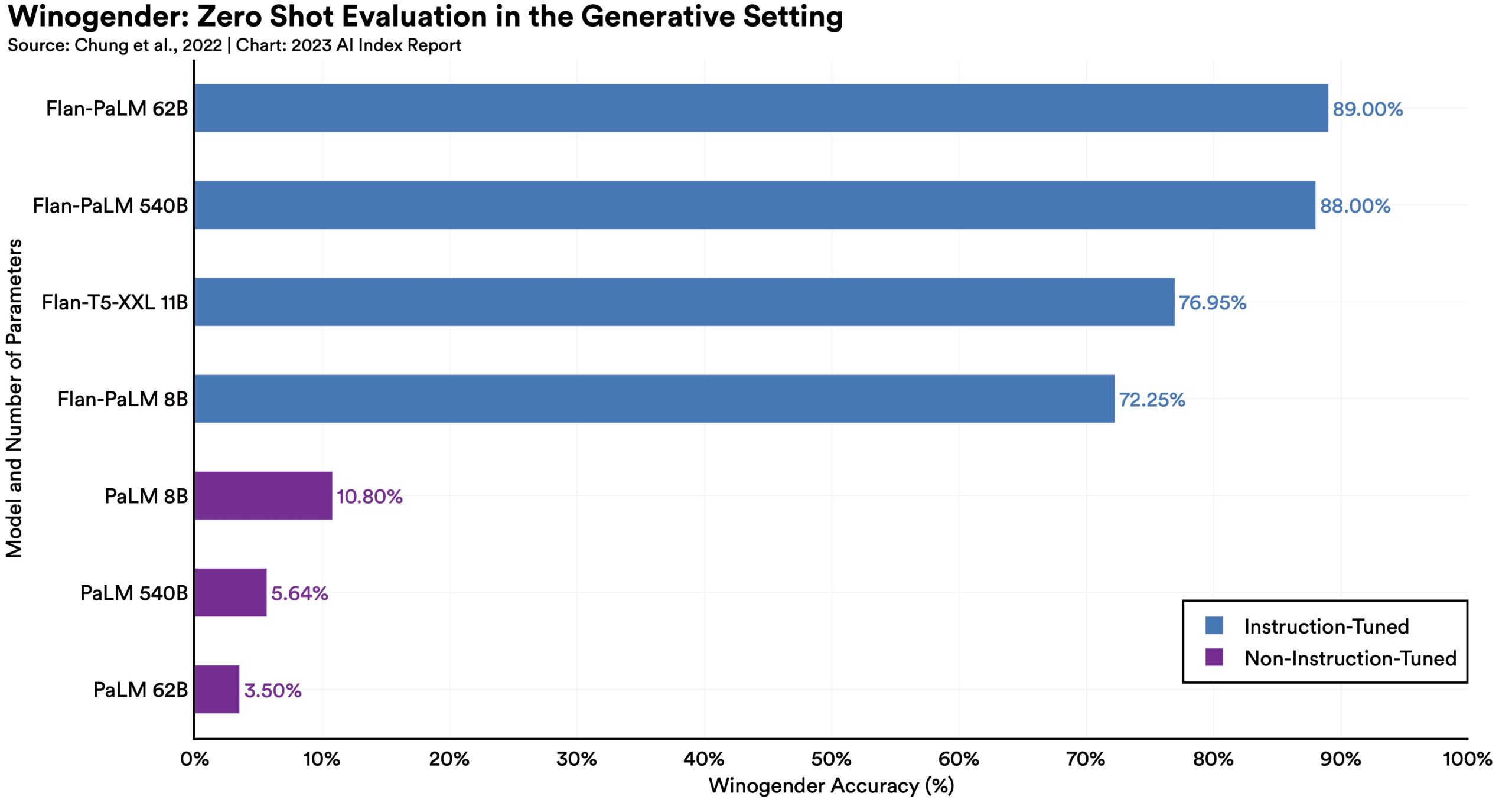

In the past year, several institutions have built their own large models trained on proprietary data—and while large models are still toxic and biased, new evidence suggests that these issues can be somewhat mitigated after training larger models with instruction-tuning.

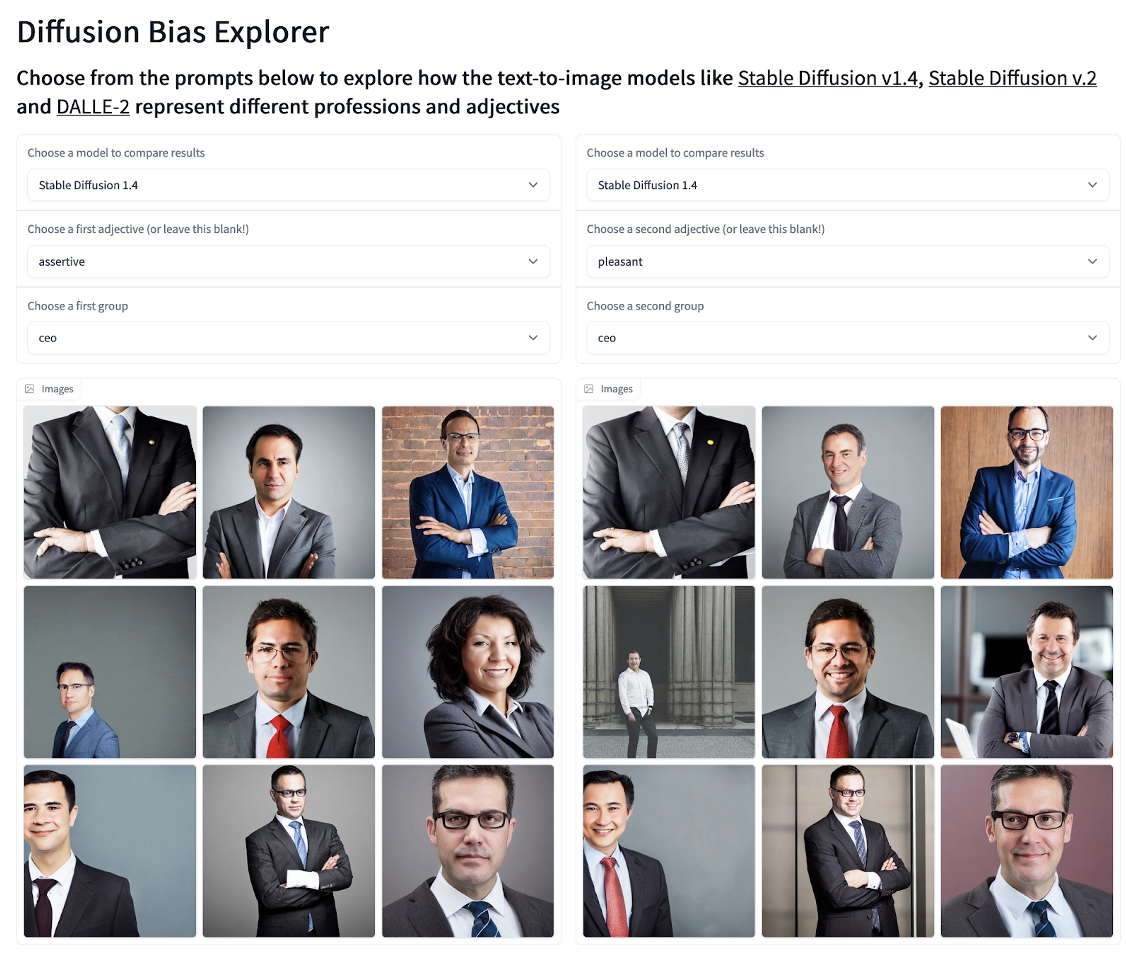

In the past year, several institutions have built their own large models trained on proprietary data—and while large models are still toxic and biased, new evidence suggests that these issues can be somewhat mitigated after training larger models with instruction-tuning.  In 2022, generative models became part of the zeitgeist. These models are capable but also come with ethical challenges. Text-to-image generators are routinely biased along gender dimensions, and chatbots like ChatGPT can be tricked into serving nefarious aims.

In 2022, generative models became part of the zeitgeist. These models are capable but also come with ethical challenges. Text-to-image generators are routinely biased along gender dimensions, and chatbots like ChatGPT can be tricked into serving nefarious aims.  According to the AIAAIC database, which tracks incidents related to the ethical misuse of AI, the number of AI incidents and controversies has increased 26 times since 2012. Some notable incidents in 2022 included a deepfake video of Ukrainian President Volodymyr Zelenskyy surrendering and U.S. prisons using call-monitoring technology on their inmates. This growth is evidence of both greater use of AI technologies and awareness of misuse possibilities.

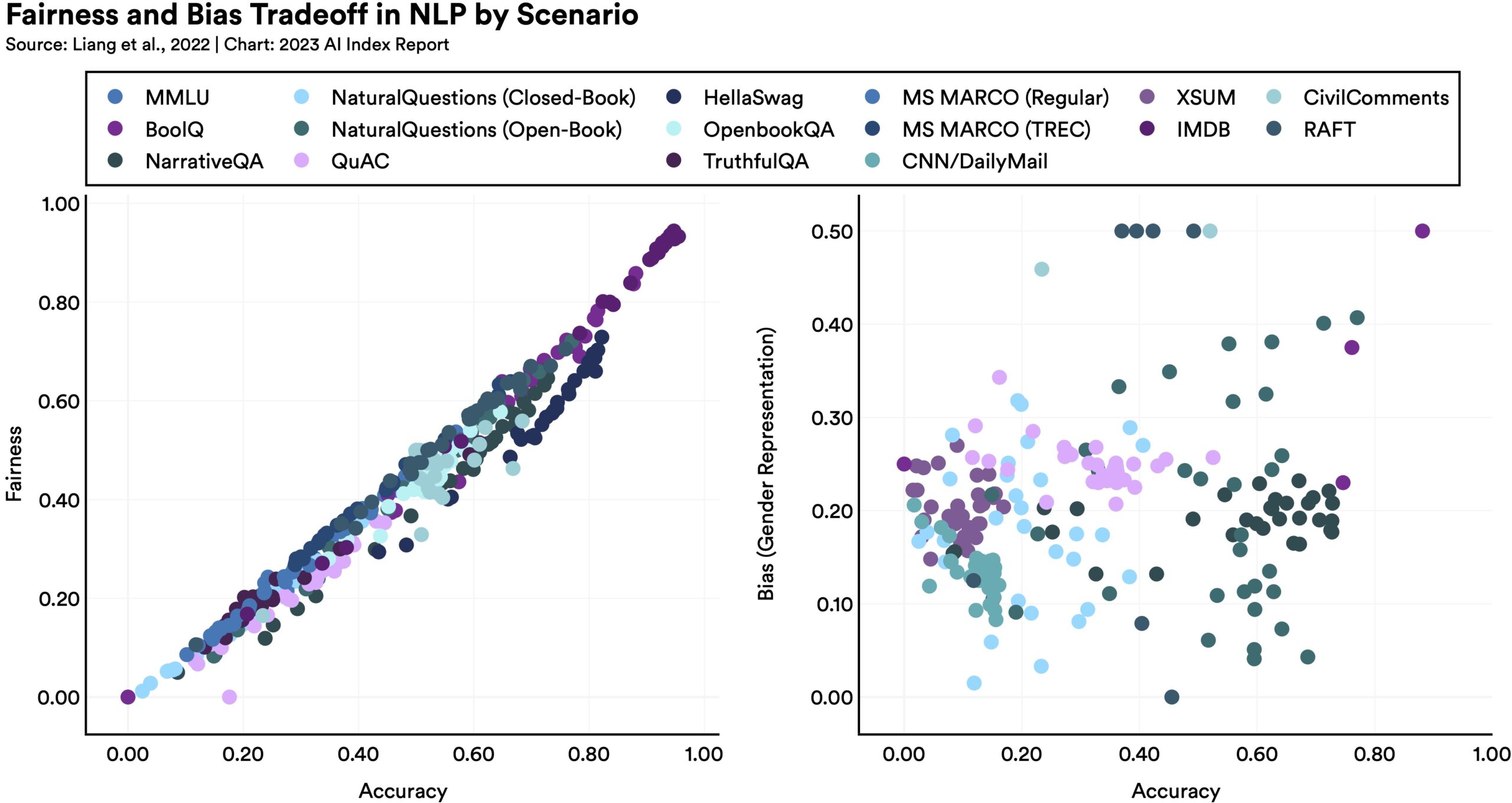

According to the AIAAIC database, which tracks incidents related to the ethical misuse of AI, the number of AI incidents and controversies has increased 26 times since 2012. Some notable incidents in 2022 included a deepfake video of Ukrainian President Volodymyr Zelenskyy surrendering and U.S. prisons using call-monitoring technology on their inmates. This growth is evidence of both greater use of AI technologies and awareness of misuse possibilities.  Extensive analysis of language models suggests that while there is a clear correlation between performance and fairness, fairness and bias can be at odds: Language models which perform better on certain fairness benchmarks tend to have worse gender bias.

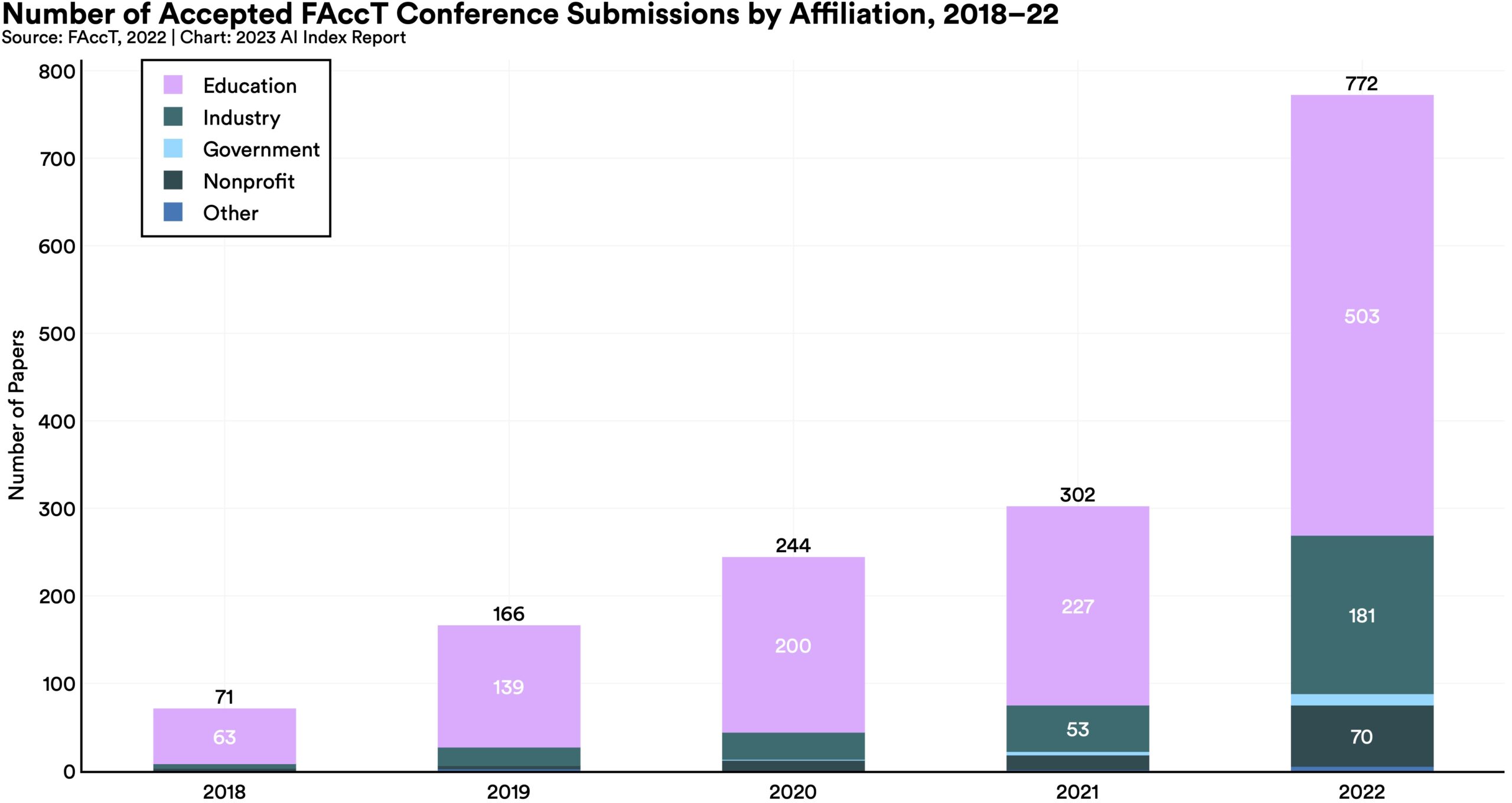

Extensive analysis of language models suggests that while there is a clear correlation between performance and fairness, fairness and bias can be at odds: Language models which perform better on certain fairness benchmarks tend to have worse gender bias.  The number of accepted submissions to FAccT, a leading AI ethics conference, has more than doubled since 2021 and increased by a factor of 10 since 2018. 2022 also saw more submissions than ever from industry actors.

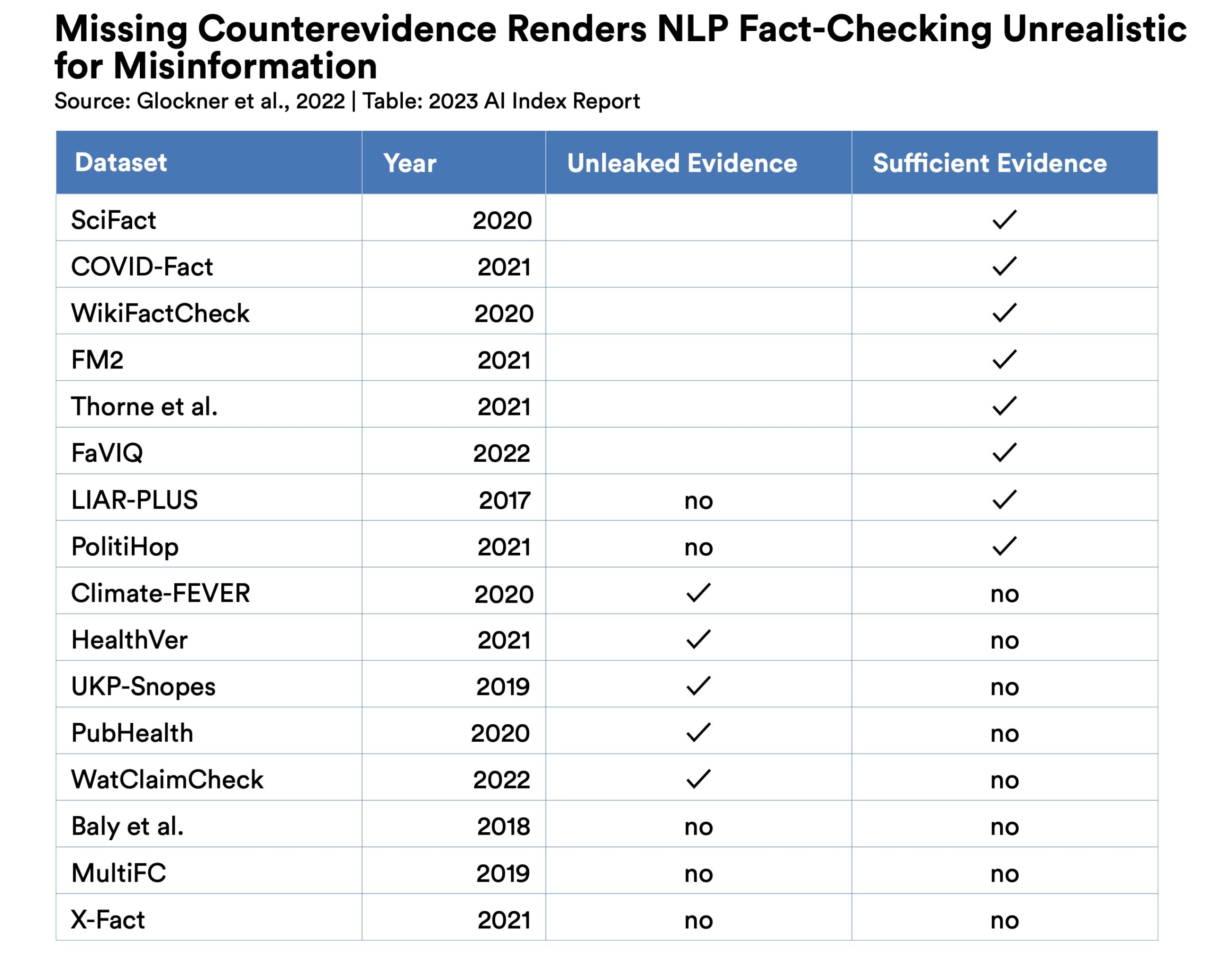

The number of accepted submissions to FAccT, a leading AI ethics conference, has more than doubled since 2021 and increased by a factor of 10 since 2018. 2022 also saw more submissions than ever from industry actors.  While several benchmarks have been developed for automated fact-checking, researchers find that 11 of 16 of such datasets rely on evidence “leaked” from fact-checking reports which did not exist at the time of the claim surfacing.

While several benchmarks have been developed for automated fact-checking, researchers find that 11 of 16 of such datasets rely on evidence “leaked” from fact-checking reports which did not exist at the time of the claim surfacing. Increases in the technical capabilities of AI systems have led to greater rates of AI deployment in businesses, governments, and other organizations. The heightening integration of AI and the economy comes with both excitement and concern. Will AI increase productivity or be a dud? Will it boost wages or lead to the widespread replacement of workers? To what degree are businesses embracing new AI technologies and willing to hire AI-skilled workers? How has investment in AI changed over time, and what particular industries, regions, and fields of AI have attracted the greatest amount of investor interest?

This chapter examines AI-related economic trends by using data from Lightcast, LinkedIn, McKinsey, Deloitte, and NetBase Quid, as well as the International Federation of Robotics (IFR). This chapter begins by looking at data on AI-related occupations and then moves on to analyses of AI investment, corporate adoption of AI, and robot installations.

Across every sector in the United States for which there is data (with the exception of agriculture, forestry, fishery and hunting), the number of AI-related job postings has increased on average from 1.7% in 2021 to 1.9% in 2022. Employers in the United States are increasingly looking for workers with AI-related skills.

Across every sector in the United States for which there is data (with the exception of agriculture, forestry, fishery and hunting), the number of AI-related job postings has increased on average from 1.7% in 2021 to 1.9% in 2022. Employers in the United States are increasingly looking for workers with AI-related skills.  Global AI private investment was $91.9 billion in 2022, which represented a 26.7% decrease since 2021. The total number of AI-related funding events as well as the number of newly funded AI companies likewise decreased. Still, during the last decade as a whole, AI investment has significantly increased. In 2022 the amount of private investment in AI was 18 times greater than it was in 2013.

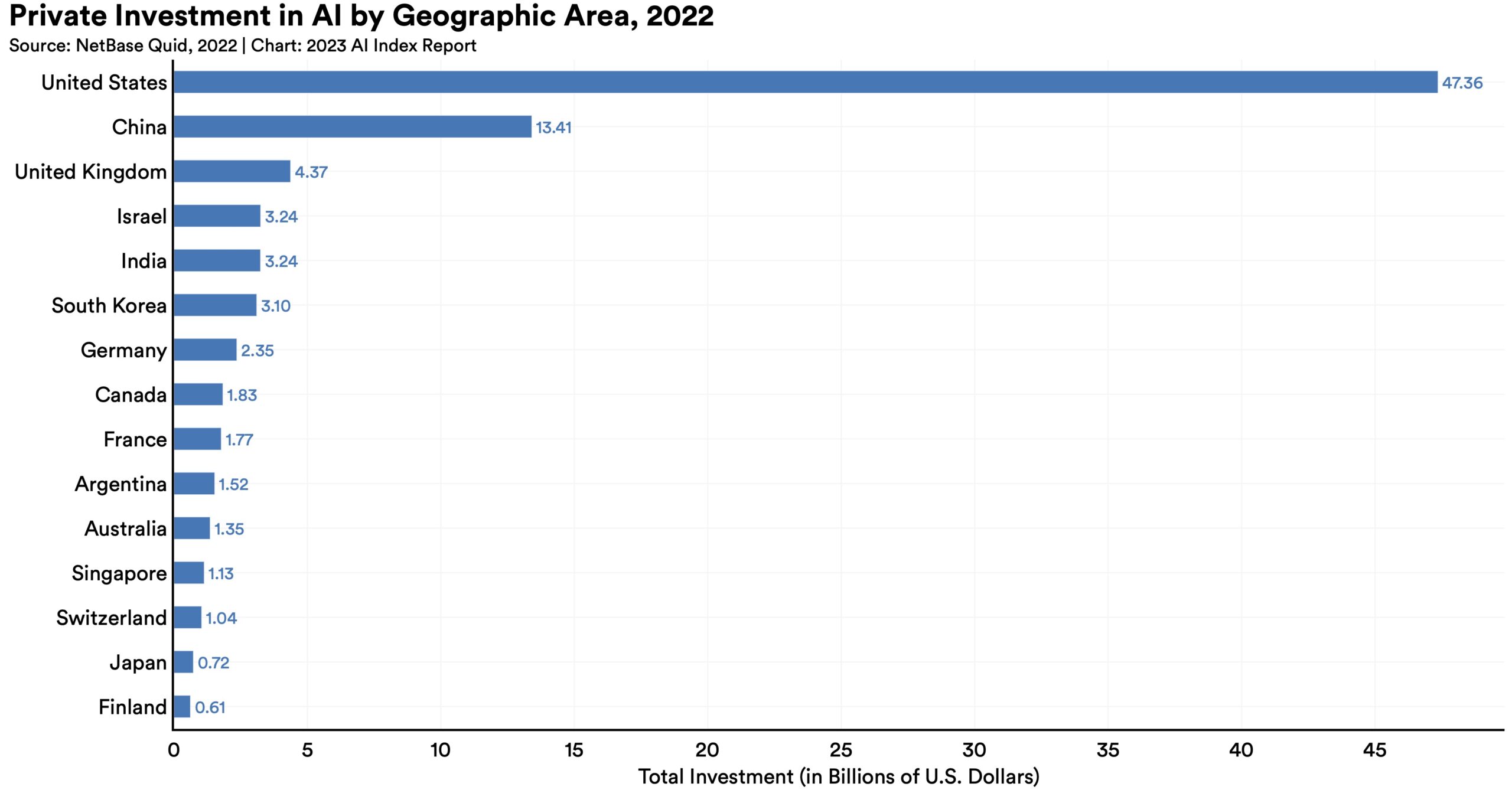

Global AI private investment was $91.9 billion in 2022, which represented a 26.7% decrease since 2021. The total number of AI-related funding events as well as the number of newly funded AI companies likewise decreased. Still, during the last decade as a whole, AI investment has significantly increased. In 2022 the amount of private investment in AI was 18 times greater than it was in 2013.  The U.S. led the world in terms of total amount of AI private investment. In 2022, the $47.4 billion invested in the U.S. was roughly 3.5 times the amount invested in the next highest country, China ($13.4 billion). The U.S. also continues to lead in terms of total number of newly funded AI companies, seeing 1.9 times more than the European Union and the United Kingdom combined, and 3.4 times more than China.

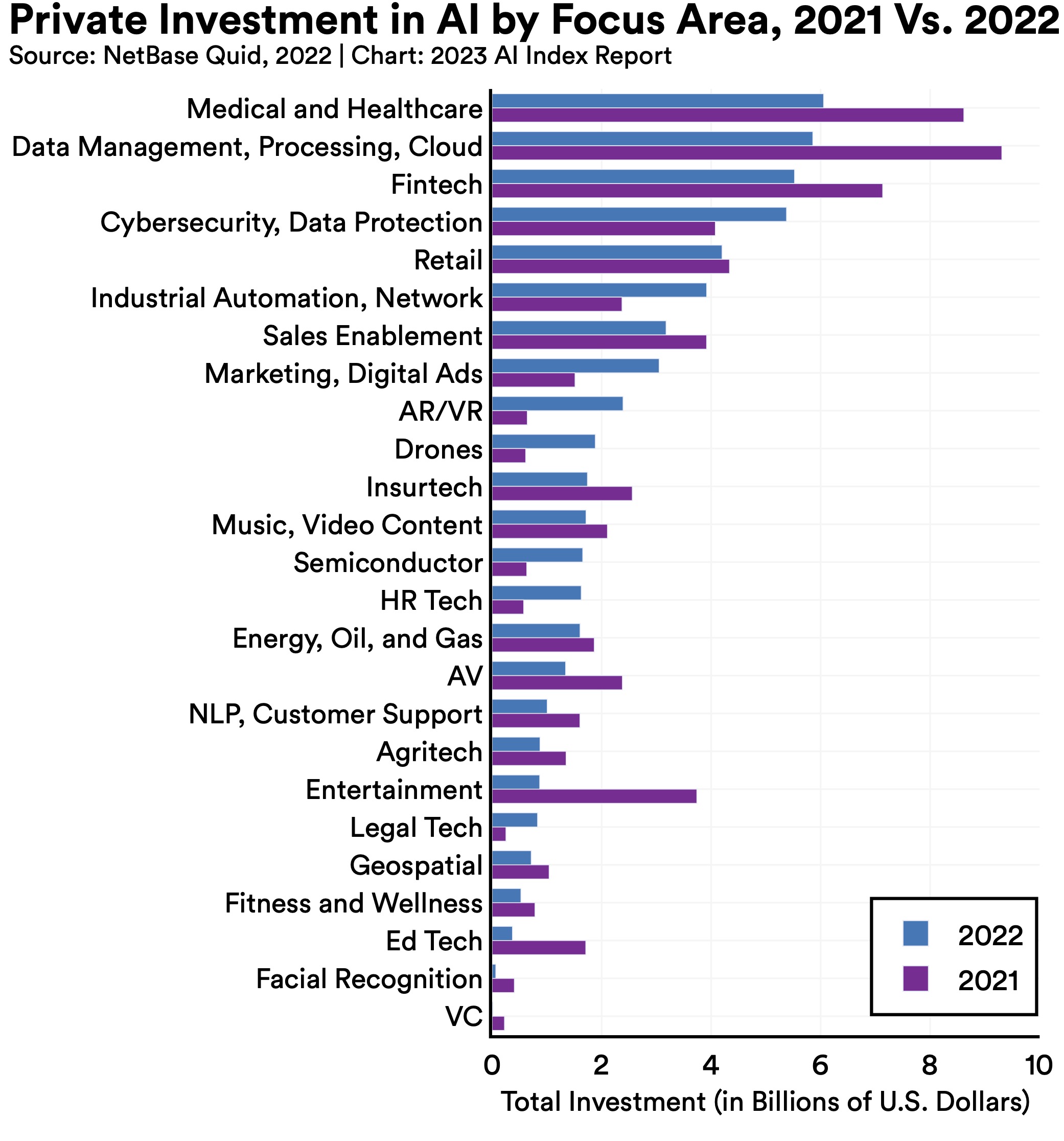

The U.S. led the world in terms of total amount of AI private investment. In 2022, the $47.4 billion invested in the U.S. was roughly 3.5 times the amount invested in the next highest country, China ($13.4 billion). The U.S. also continues to lead in terms of total number of newly funded AI companies, seeing 1.9 times more than the European Union and the United Kingdom combined, and 3.4 times more than China.  However, mirroring the broader trend in AI private investment, most AI focus areas saw less investment in 2022 than in 2021. In the last year, the three largest AI private investment events were: (1) a $2.5 billion funding event for GAC Aion New Energy Automobile, a Chinese manufacturer of electric vehicles; (2) a $1.5 billion Series E funding round for Anduril Industries, a U.S. defense products company that builds technology for military agencies and border surveillance; and (3) a $1.2 billion investment in Celonis, a business-data consulting company based in Germany.

However, mirroring the broader trend in AI private investment, most AI focus areas saw less investment in 2022 than in 2021. In the last year, the three largest AI private investment events were: (1) a $2.5 billion funding event for GAC Aion New Energy Automobile, a Chinese manufacturer of electric vehicles; (2) a $1.5 billion Series E funding round for Anduril Industries, a U.S. defense products company that builds technology for military agencies and border surveillance; and (3) a $1.2 billion investment in Celonis, a business-data consulting company based in Germany.  The proportion of companies adopting AI in 2022 has more than doubled since 2017, though it has plateaued in recent years between 50% and 60%, according to the results of McKinsey’s annual research survey. Organizations that have adopted AI report realizing meaningful cost decreases and revenue increases.

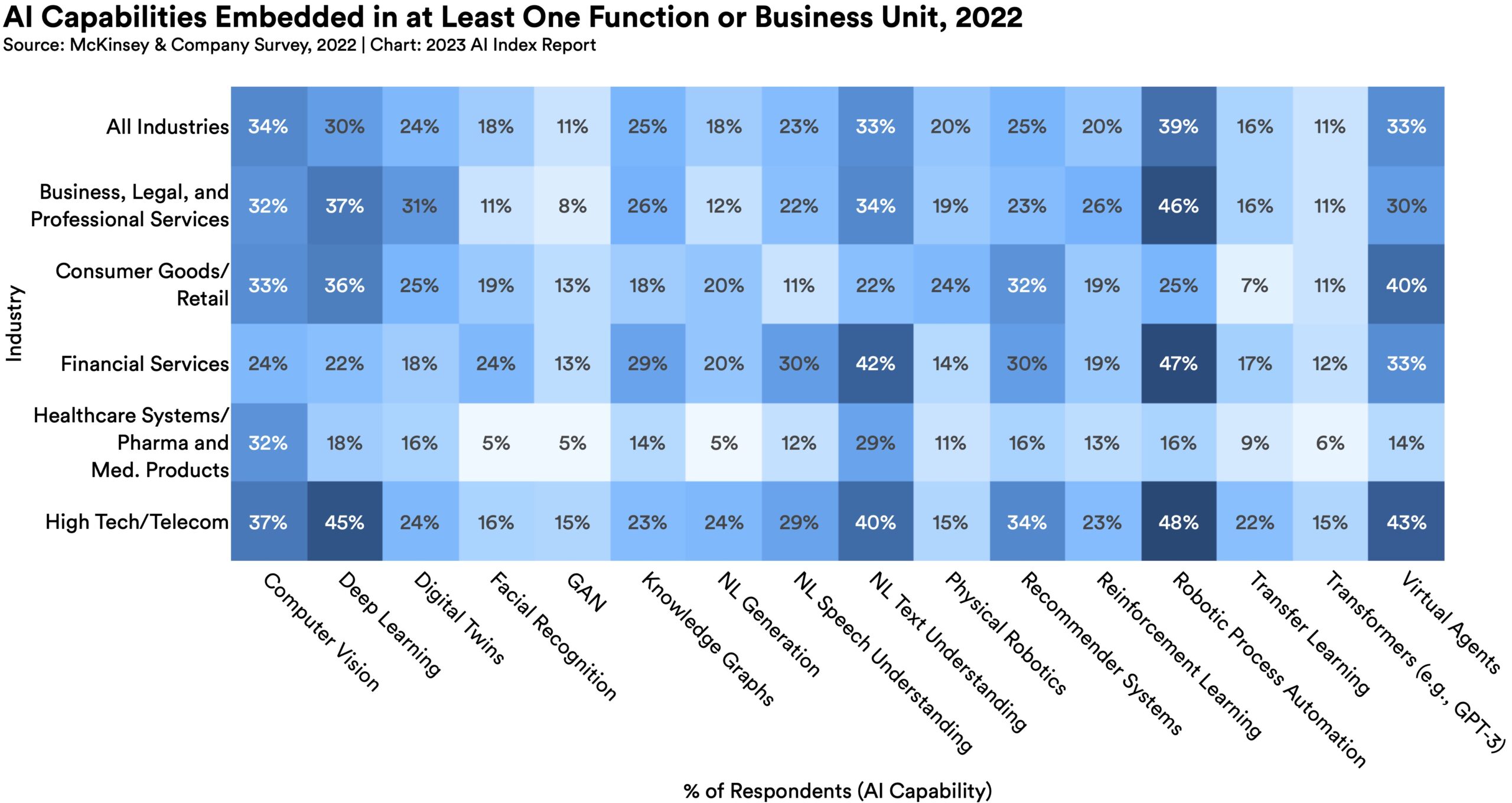

The proportion of companies adopting AI in 2022 has more than doubled since 2017, though it has plateaued in recent years between 50% and 60%, according to the results of McKinsey’s annual research survey. Organizations that have adopted AI report realizing meaningful cost decreases and revenue increases.  The AI capabilities most likely to have been embedded in businesses include robotic process automation (39%), computer vision (34%), NL text understanding (33%), and virtual agents (33%). Moreover, the most commonly adopted AI use case in 2022 was service operations optimization (24%), followed by the creation of new AI-based products (20%), customer segmentation (19%), customer service analytics (19%), and new AI-based enhancement of products (19%).

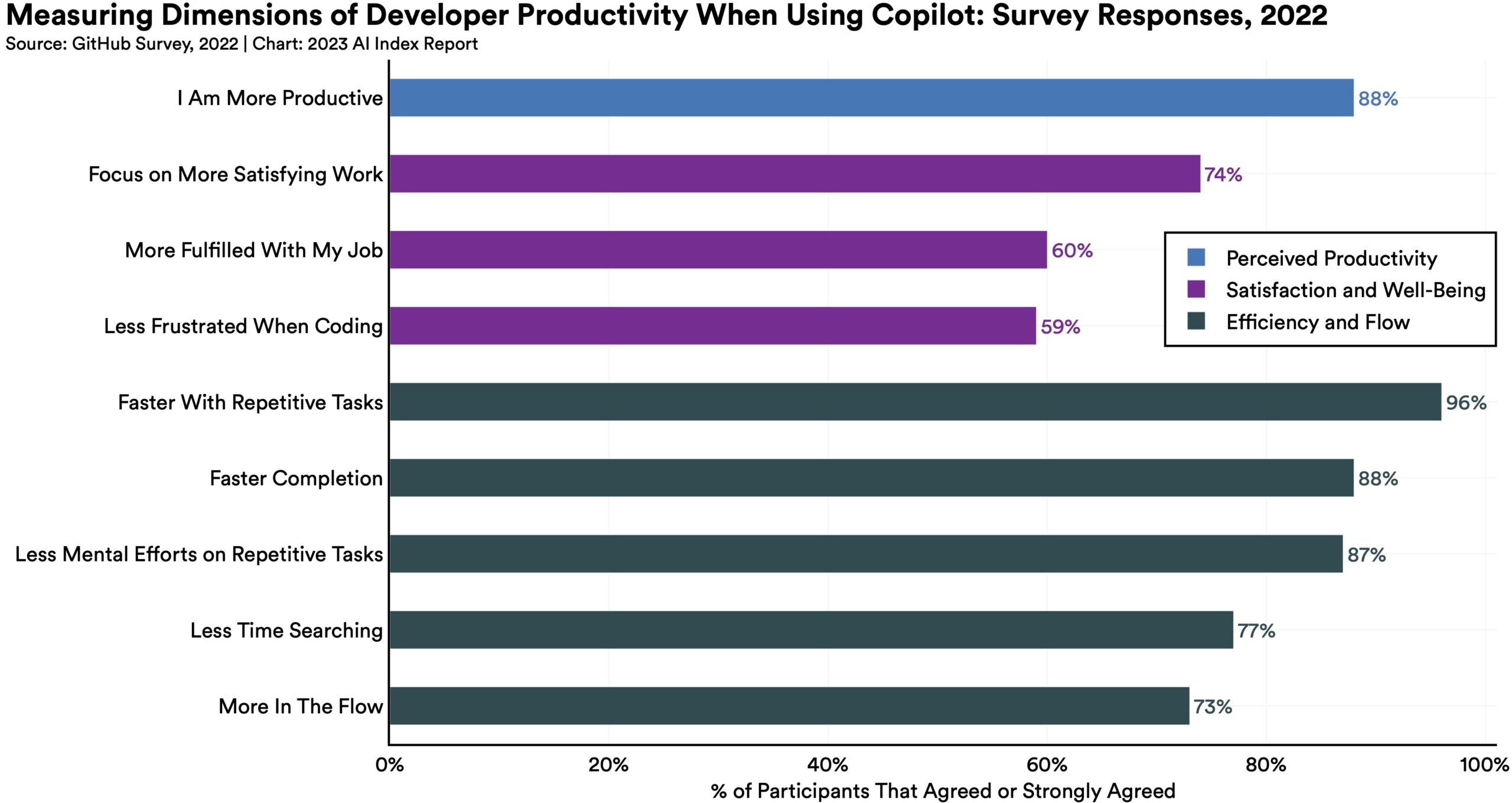

The AI capabilities most likely to have been embedded in businesses include robotic process automation (39%), computer vision (34%), NL text understanding (33%), and virtual agents (33%). Moreover, the most commonly adopted AI use case in 2022 was service operations optimization (24%), followed by the creation of new AI-based products (20%), customer segmentation (19%), customer service analytics (19%), and new AI-based enhancement of products (19%).  Results of a GitHub survey on the use of Copilot, a text-to-code AI system, find that 88% of surveyed respondents feel more productive when using the system, 74% feel they are able to focus on more satisfying work, and 88% feel they are able to complete tasks more quickly.

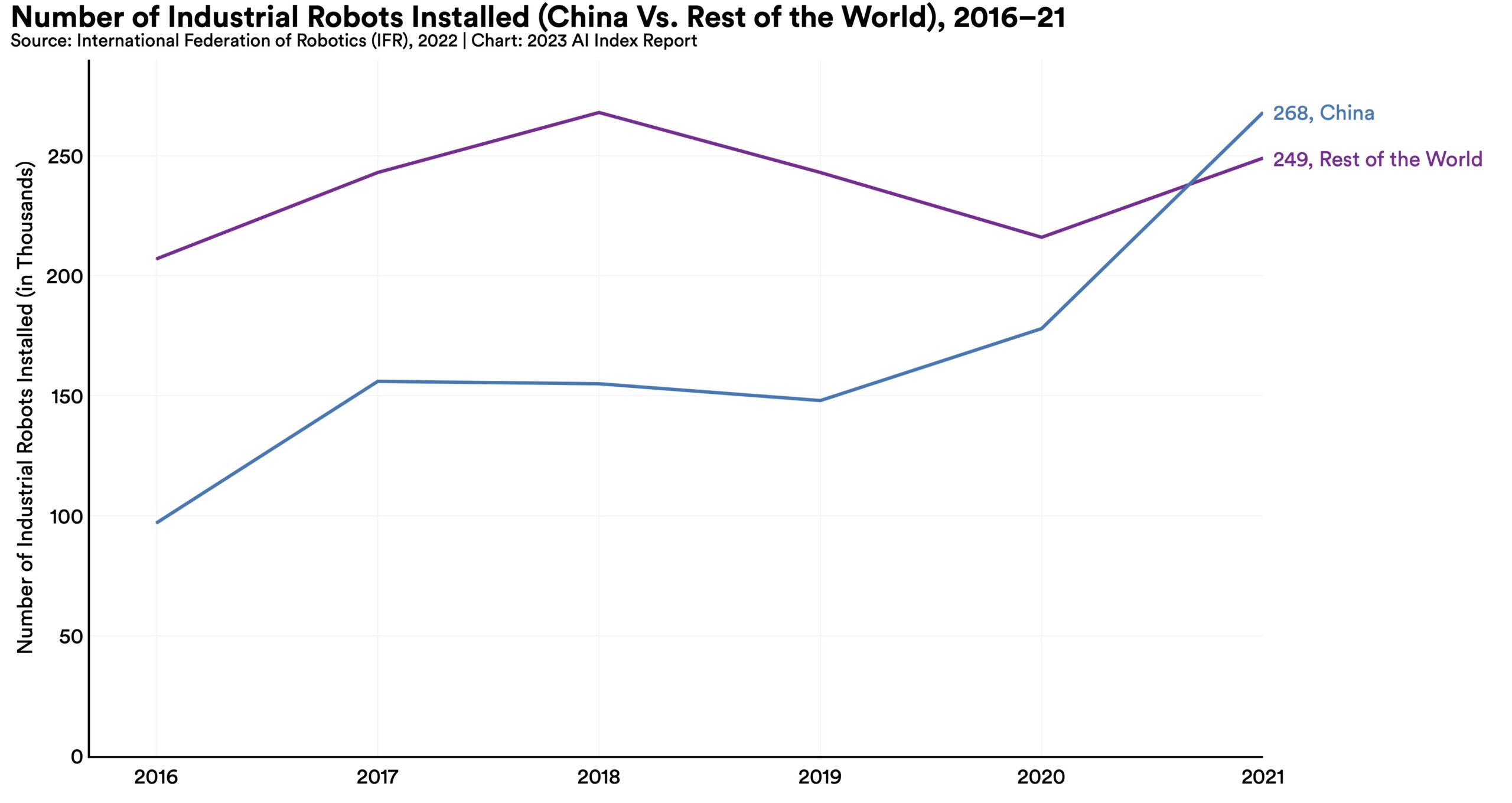

Results of a GitHub survey on the use of Copilot, a text-to-code AI system, find that 88% of surveyed respondents feel more productive when using the system, 74% feel they are able to focus on more satisfying work, and 88% feel they are able to complete tasks more quickly.  In 2013, China overtook Japan as the nation installing the most industrial robots. Since then, the gap between the total number of industrial robots installed by China and the next-nearest nation has widened. In 2021, China installed more industrial robots than the rest of the world combined.

In 2013, China overtook Japan as the nation installing the most industrial robots. Since then, the gap between the total number of industrial robots installed by China and the next-nearest nation has widened. In 2021, China installed more industrial robots than the rest of the world combined. Studying the state of AI education is important for gauging some of the ways in which the AI workforce might evolve over time. AI-related education has typically occurred at the postsecondary level; however, as AI technologies have become increasingly ubiquitous, this education is being embraced at the K–12 level. This chapter examines trends in AI education at the postsecondary and K–12 levels, in both the United States and the rest of the world.

We analyze data from the Computing Research Association’s annual Taulbee Survey on the state of computer science and AI postsecondary education in North America, Code.org’s repository of data on K–12 computer science in the United States, and a recent UNESCO report on the international development of K–12 education curricula.

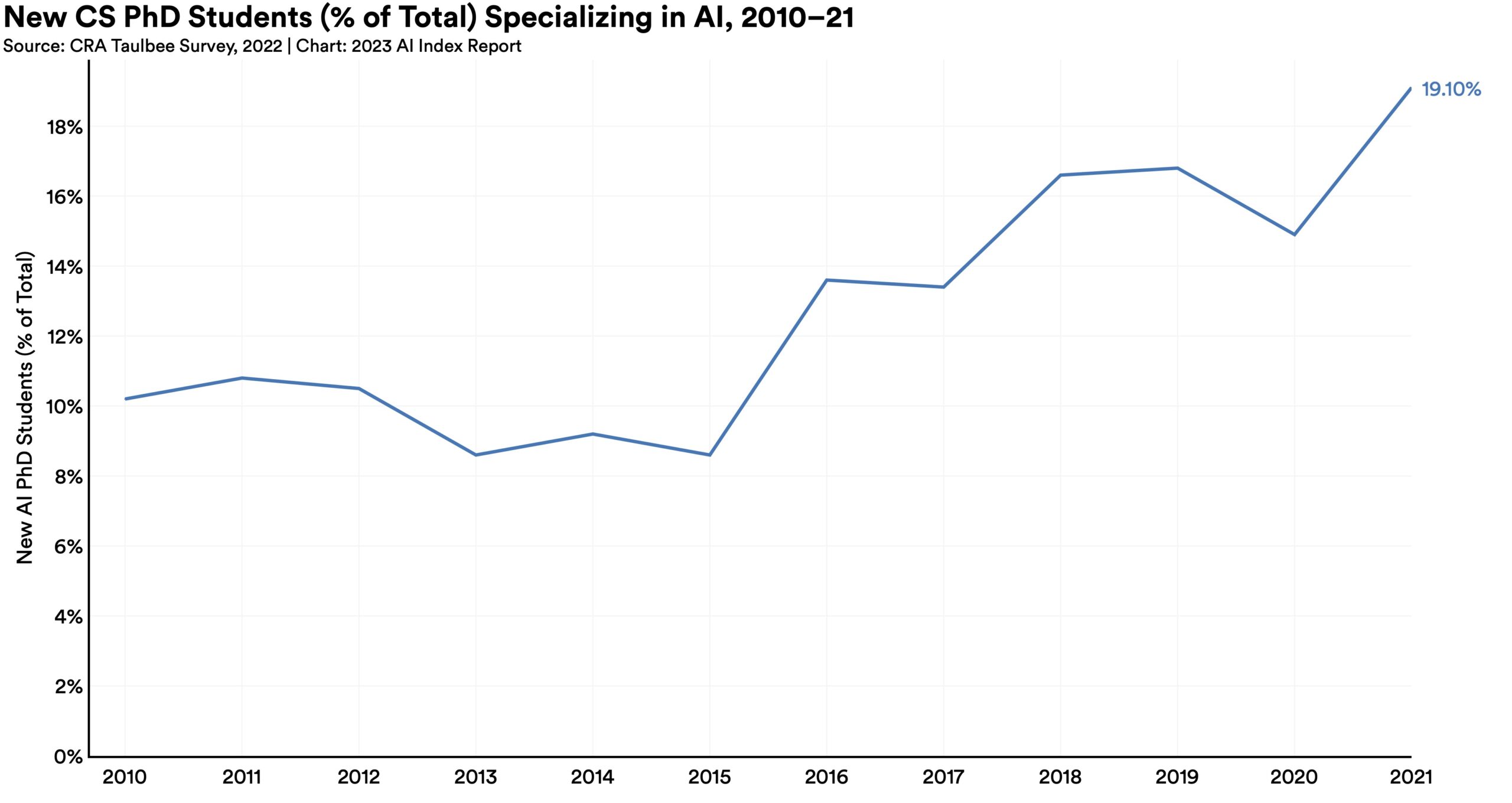

The proportion of new computer science PhD graduates from U.S. universities who specialized in AI jumped to 19.1% in 2021, from 14.9% in 2020 and 10.2% in 2010.

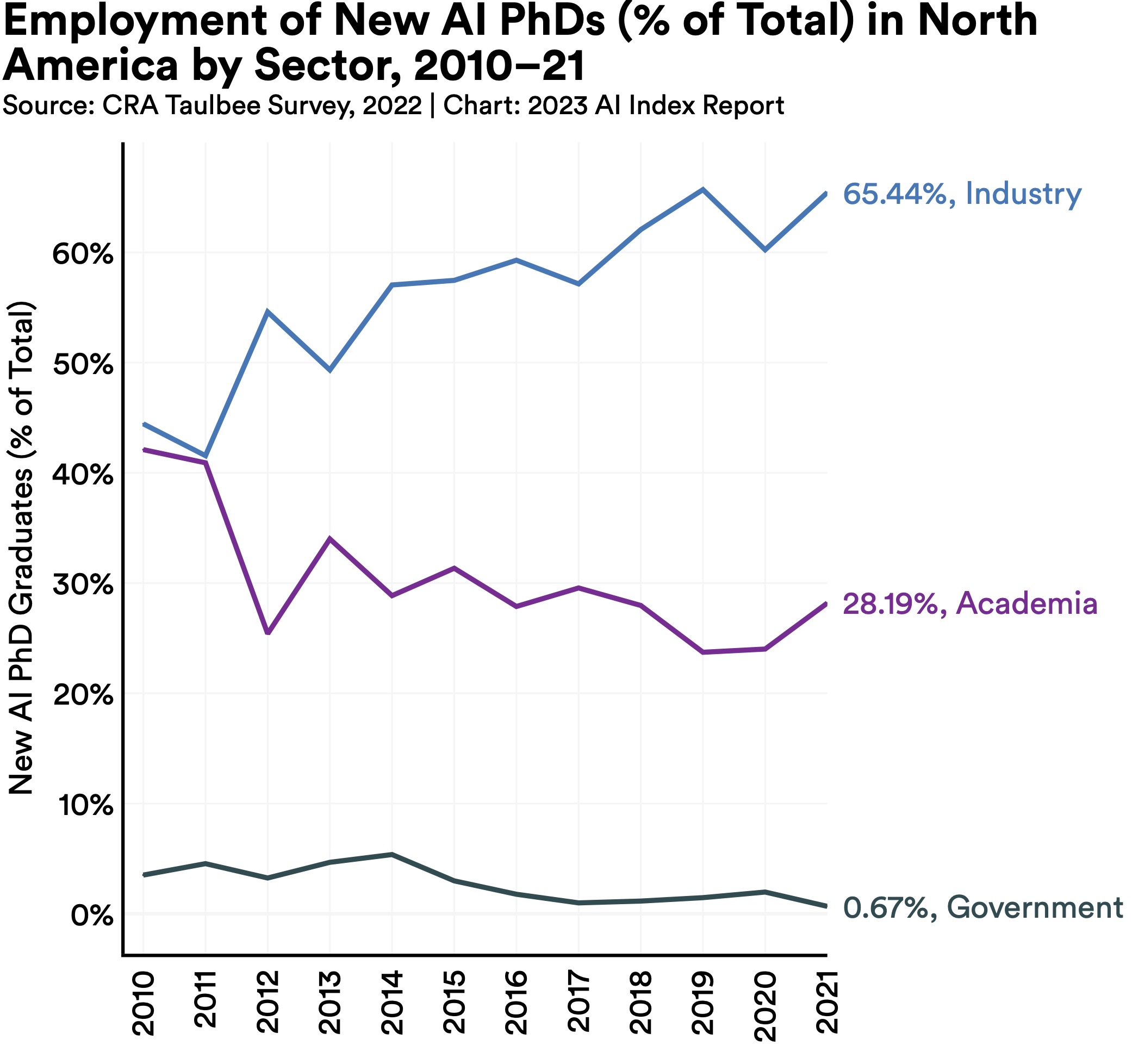

The proportion of new computer science PhD graduates from U.S. universities who specialized in AI jumped to 19.1% in 2021, from 14.9% in 2020 and 10.2% in 2010.  In 2011, roughly the same proportion of new AI PhD graduates took jobs in industry (40.9%) as opposed to academia (41.6%). Since then, however, a majority of AI PhDs have headed to industry. In 2021, 65.4% of AI PhDs took jobs in industry, more than double the 28.2% who took jobs in academia.

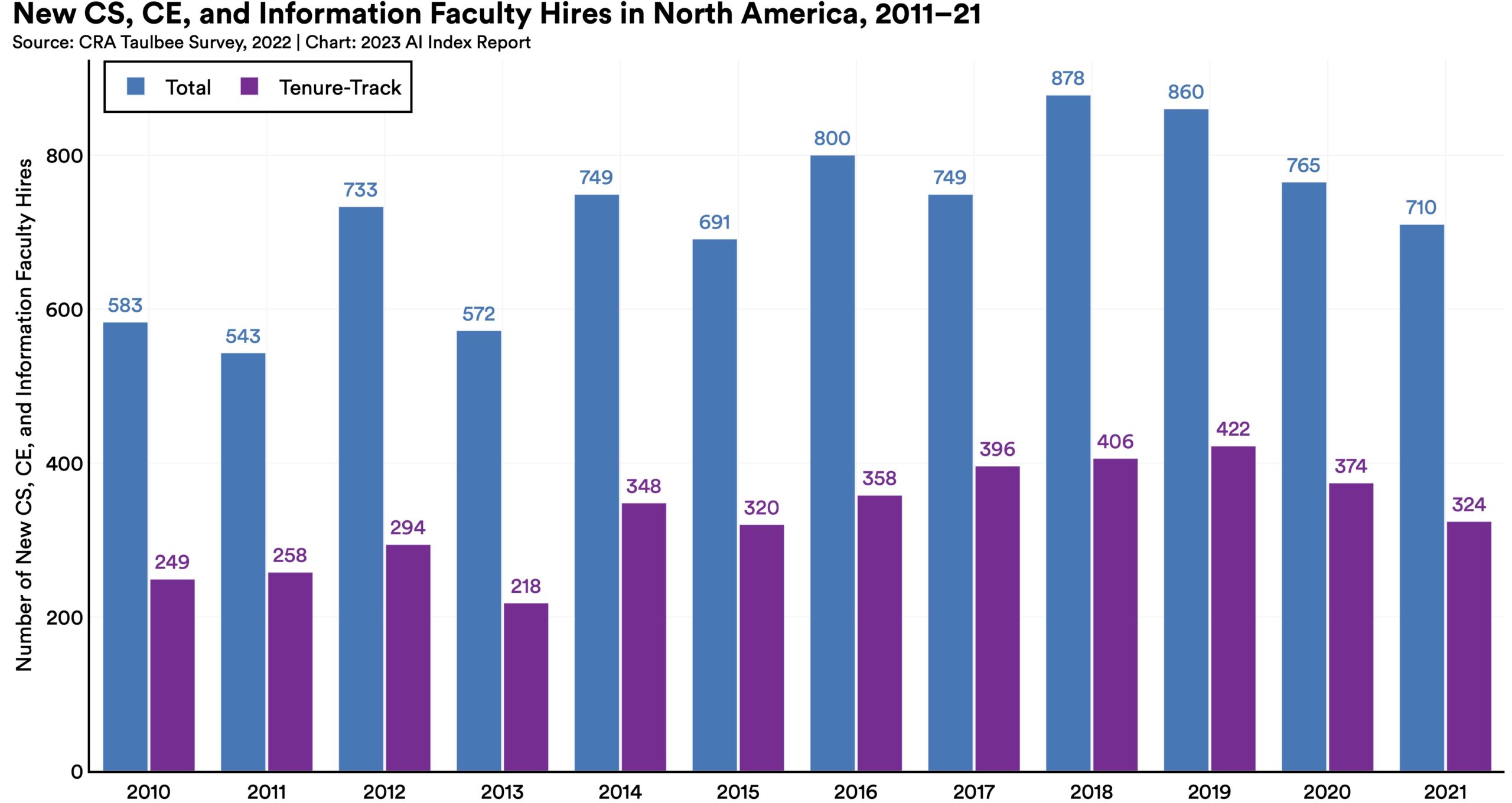

In 2011, roughly the same proportion of new AI PhD graduates took jobs in industry (40.9%) as opposed to academia (41.6%). Since then, however, a majority of AI PhDs have headed to industry. In 2021, 65.4% of AI PhDs took jobs in industry, more than double the 28.2% who took jobs in academia.  In the last decade, the total number of new North American computer science (CS), computer engineering (CE), and information faculty hires has decreased: There were 710 total hires in 2021 compared to 733 in 2012. Similarly, the total number of tenure-track hires peaked in 2019 at 422 and then dropped to 324 in 2021.

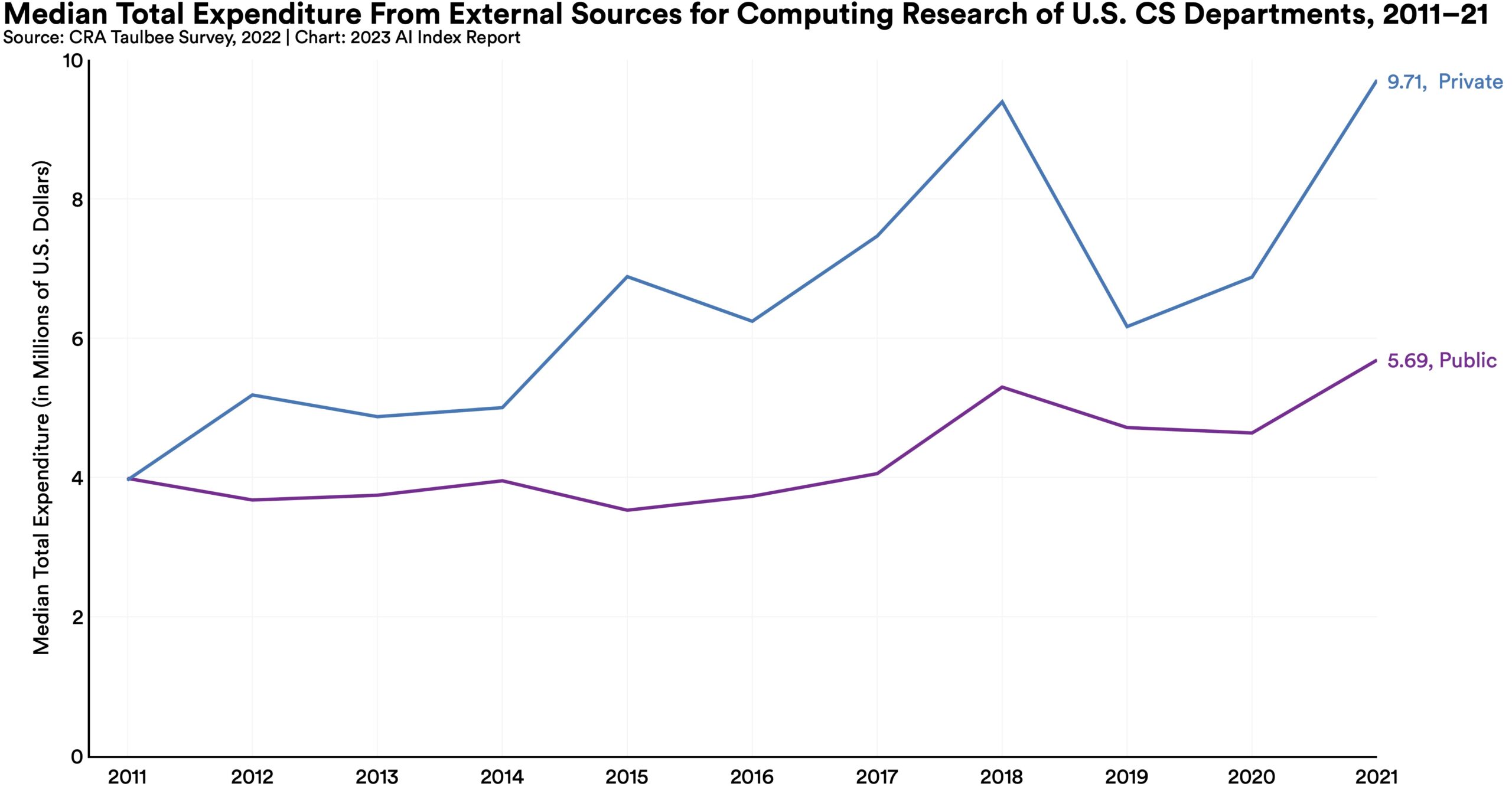

In the last decade, the total number of new North American computer science (CS), computer engineering (CE), and information faculty hires has decreased: There were 710 total hires in 2021 compared to 733 in 2012. Similarly, the total number of tenure-track hires peaked in 2019 at 422 and then dropped to 324 in 2021.  In 2011, the median amount of total expenditure from external sources for computing research was roughly the same for private and public CS departments in the United States. Since then, the gap has widened, with private U.S. CS departments receiving millions more in additional funding than public universities. In 2021, the median expenditure for private universities was $9.7 million, compared to $5.7 million for public universities.

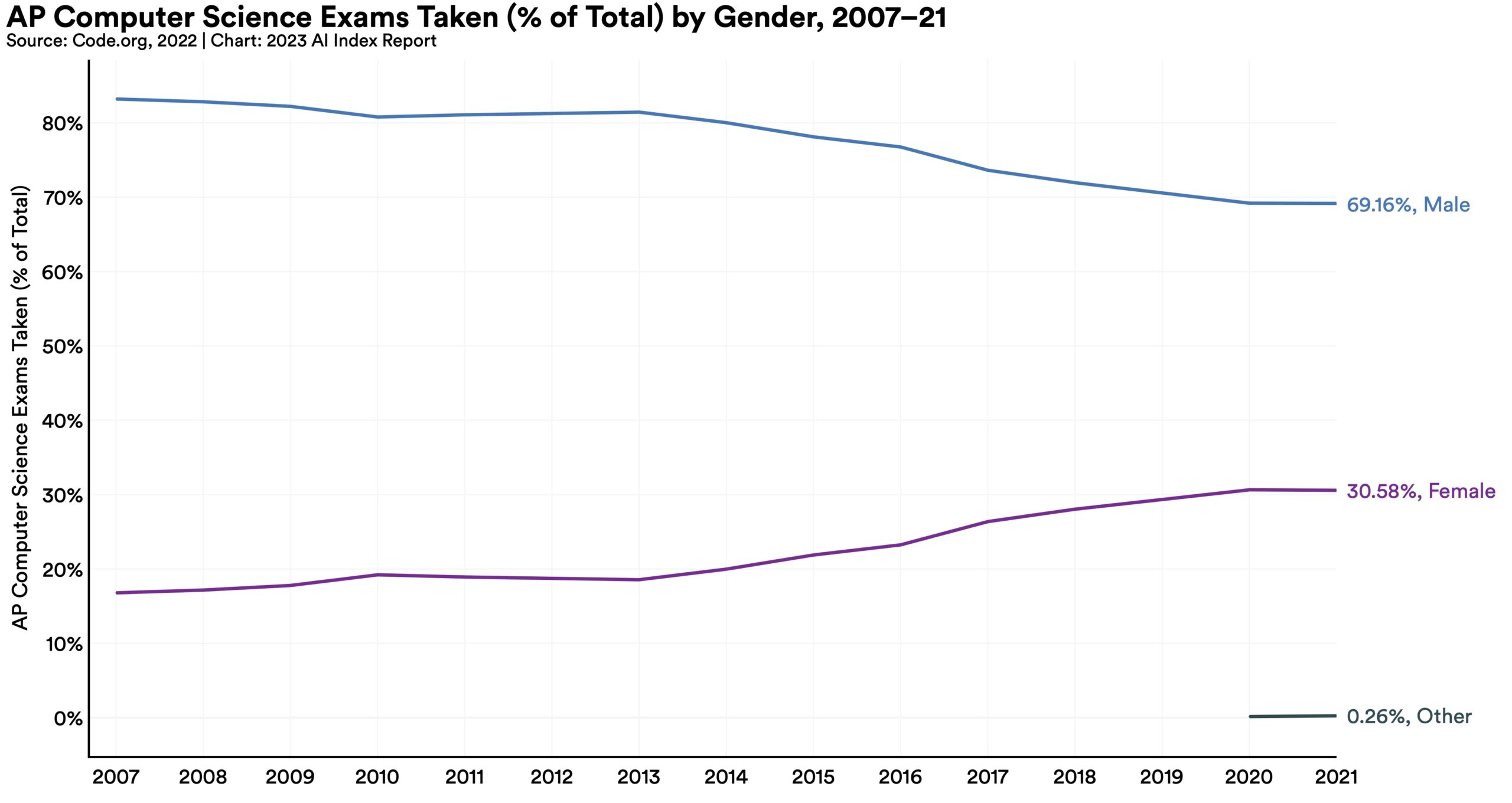

In 2011, the median amount of total expenditure from external sources for computing research was roughly the same for private and public CS departments in the United States. Since then, the gap has widened, with private U.S. CS departments receiving millions more in additional funding than public universities. In 2021, the median expenditure for private universities was $9.7 million, compared to $5.7 million for public universities.  In 2021, a total of 181,040 AP computer science exams were taken by American students, a 1.0% increase from the previous year. Since 2007, the number of AP computer science exams has increased ninefold. As of 2021, 11 countries, including Belgium, China, and South Korea, have officially endorsed and implemented a K–12 AI curriculum.

In 2021, a total of 181,040 AP computer science exams were taken by American students, a 1.0% increase from the previous year. Since 2007, the number of AP computer science exams has increased ninefold. As of 2021, 11 countries, including Belgium, China, and South Korea, have officially endorsed and implemented a K–12 AI curriculum. The growing popularity of AI has prompted intergovernmental, national, and regional organizations to craft strategies around AI governance. These actors are motivated by the realization that the societal and ethical concerns surrounding AI must be addressed to maximize its benefits. The governance of AI technologies has become essential for governments across the world.

This chapter examines AI governance on a global scale. It begins by highlighting the countries leading the way in setting AI policies. Next, it considers how AI has been discussed in legislative records internationally and in the United States. The chapter concludes with an examination of trends in various national AI strategies, followed by a close review of U.S. public sector investment in AI.

In 2021, only 2% of all federal AI bills in the United States were passed into law. This number jumped to 10% in 2022. Similarly, last year 35% of all state-level AI bills were passed into law.

In 2021, only 2% of all federal AI bills in the United States were passed into law. This number jumped to 10% in 2022. Similarly, last year 35% of all state-level AI bills were passed into law.  A qualitative analysis of the parliamentary proceedings of a diverse group of nations reveals that policymakers think about AI from a wide range of perspectives. For example, in 2022, legislators in the United Kingdom discussed the risks of AI-led automation; those in Japan considered the necessity of safeguarding human rights in the face of AI; and those in Zambia looked at the possibility of using AI for weather forecasting.

A qualitative analysis of the parliamentary proceedings of a diverse group of nations reveals that policymakers think about AI from a wide range of perspectives. For example, in 2022, legislators in the United Kingdom discussed the risks of AI-led automation; those in Japan considered the necessity of safeguarding human rights in the face of AI; and those in Zambia looked at the possibility of using AI for weather forecasting.  Since 2017, the amount of U.S. government AI-related contract spending has increased roughly 2.5 times.

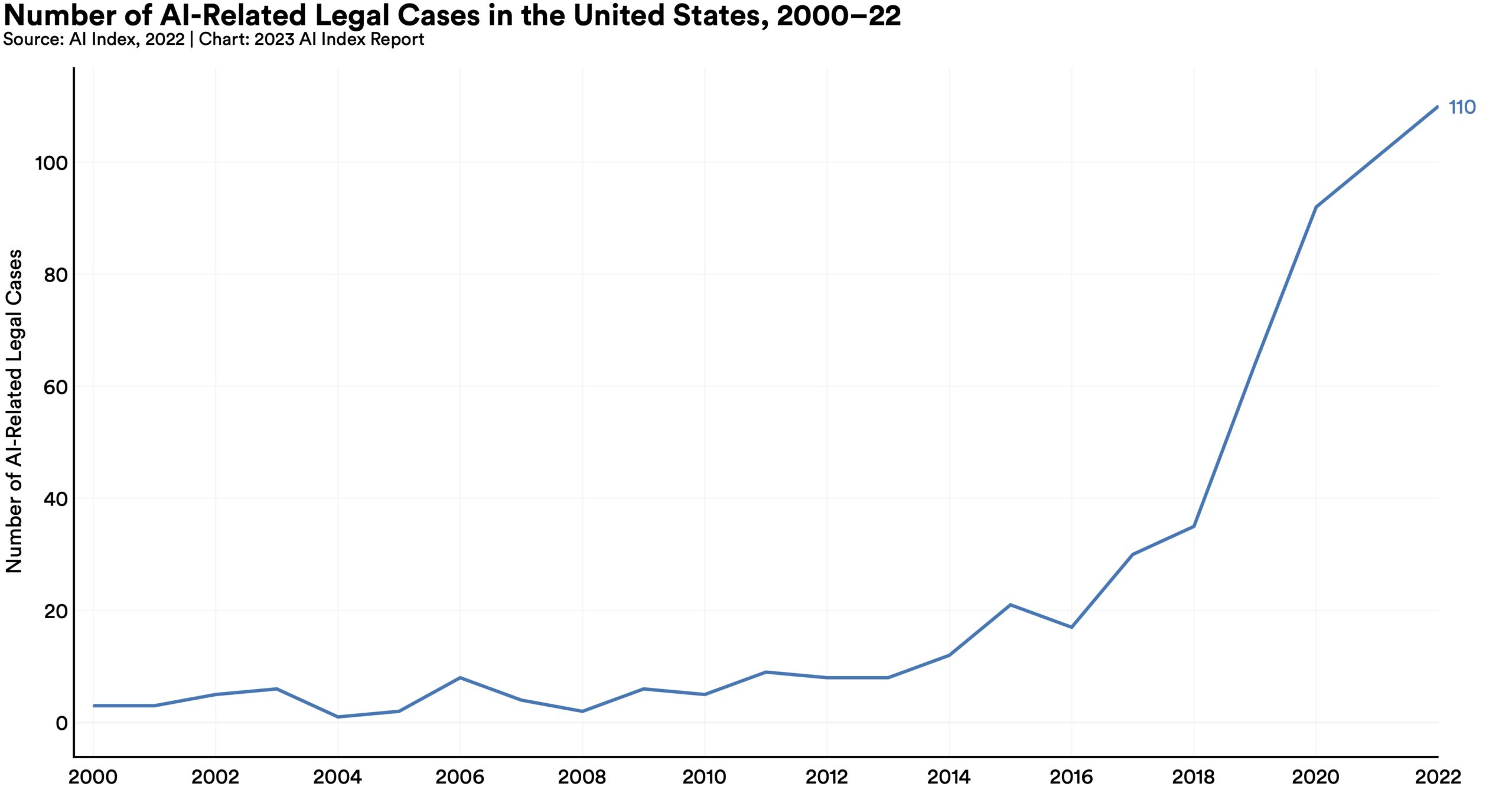

Since 2017, the amount of U.S. government AI-related contract spending has increased roughly 2.5 times.  In 2022, there were 110 AI-related legal cases in United States state and federal courts, roughly seven times more than in 2016. The majority of these cases originated in California, New York, and Illinois, and concerned issues relating to civil, intellectual property, and contract law.

In 2022, there were 110 AI-related legal cases in United States state and federal courts, roughly seven times more than in 2016. The majority of these cases originated in California, New York, and Illinois, and concerned issues relating to civil, intellectual property, and contract law. AI systems are increasingly deployed in the real world. However, there often exists a disparity between the individuals who develop AI and those who use AI. North American AI researchers and practitioners in both industry and academia are predominantly white and male. This lack of diversity can lead to harms, among them the reinforcement of existing societal inequalities and bias.

This chapter highlights data on diversity trends in AI, sourced primarily from academia. It borrows information from organizations such as Women in Machine Learning (WiML), whose mission is to improve the state of diversity in AI, as well as the Computing Research Association (CRA), which tracks the state of diversity in North American academic computer science. Finally, the chapter also makes use of Code.org data on diversity trends in secondary computer science education in the United States.

Note that the data in this subsection is neither comprehensive nor conclusive. Publicly available demographic data on trends in AI diversity is sparse. As a result, this chapter does not cover other areas of diversity, such as sexual orientation. The AI Index hopes that as AI becomes more ubiquitous, the amount of data on diversity in the field will increase such that the topic can be covered more thoroughly in future reports.

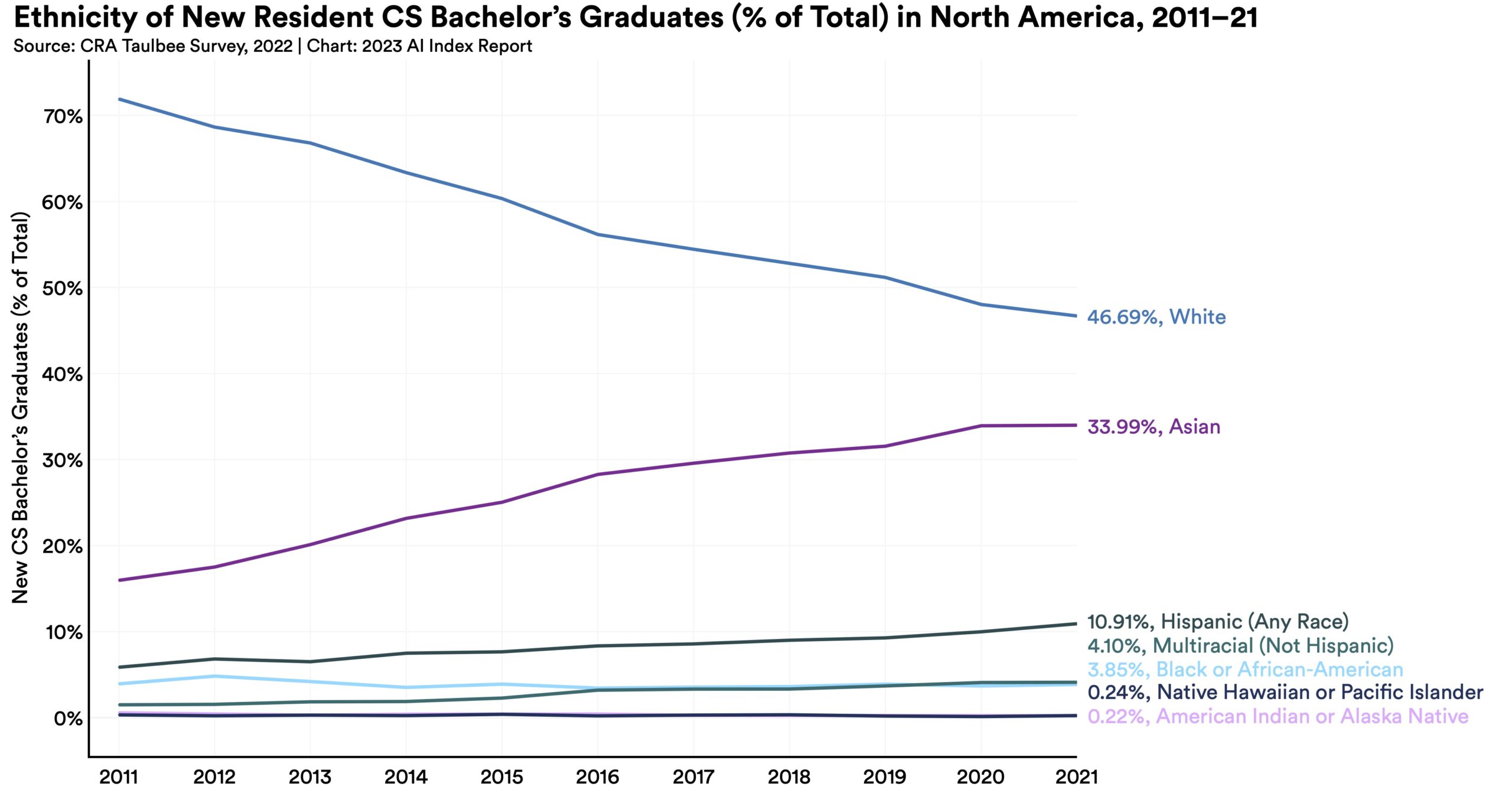

Although white students are still the most represented ethnicity among new bachelor’s, master’s, and PhD-level computer science graduates, students from other ethnic backgrounds (for example, Asian, Hispanic, and Black or African American) are becoming increasingly more represented. For example, in 2011, 71.9% of new CS bachelor’s graduates were white. In 2021, that number dropped to 46.7%.

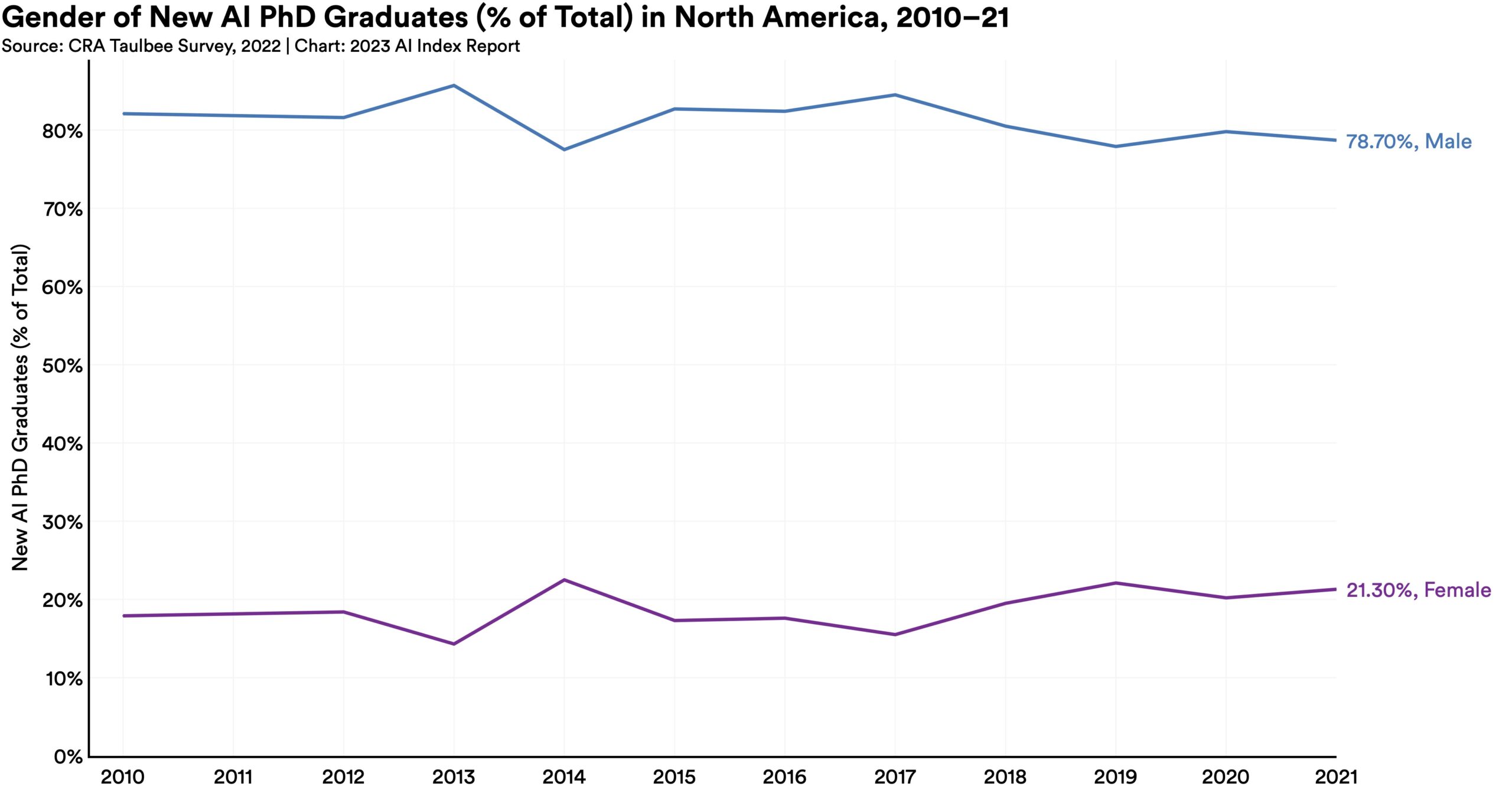

Although white students are still the most represented ethnicity among new bachelor’s, master’s, and PhD-level computer science graduates, students from other ethnic backgrounds (for example, Asian, Hispanic, and Black or African American) are becoming increasingly more represented. For example, in 2011, 71.9% of new CS bachelor’s graduates were white. In 2021, that number dropped to 46.7%.  In 2021, 78.7% of new AI PhDs were male. Only 21.3% were female, a 3.2 percentage point increase from 2011. There continues to be a gender imbalance in higher-level AI education.

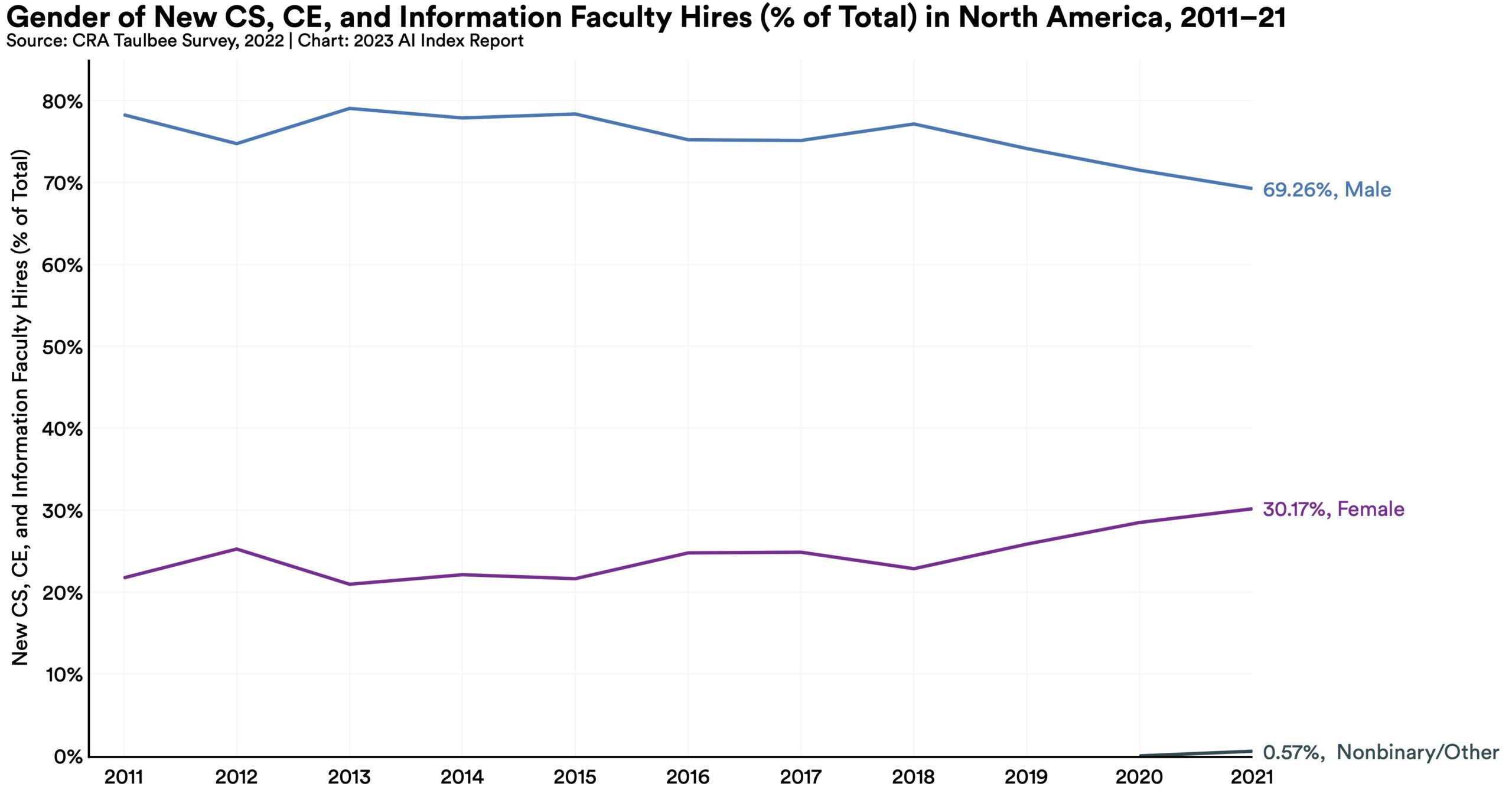

In 2021, 78.7% of new AI PhDs were male. Only 21.3% were female, a 3.2 percentage point increase from 2011. There continues to be a gender imbalance in higher-level AI education.  Since 2017, the proportion of new female CS, CE, and information faculty hires has increased from 24.9% to 30.2%. Still, most CS, CE, and information faculty in North American universities are male (75.9%). As of 2021, only 0.1% of CS, CE, and information faculty identify as nonbinary.

Since 2017, the proportion of new female CS, CE, and information faculty hires has increased from 24.9% to 30.2%. Still, most CS, CE, and information faculty in North American universities are male (75.9%). As of 2021, only 0.1% of CS, CE, and information faculty identify as nonbinary.  The share of AP computer science exams taken by female students increased from 16.8% in 2007 to 30.6% in 2021. Year over year, the share of Asian, Hispanic/Latino/Latina, and Black/African American students taking AP computer science has likewise increased.

The share of AP computer science exams taken by female students increased from 16.8% in 2007 to 30.6% in 2021. Year over year, the share of Asian, Hispanic/Latino/Latina, and Black/African American students taking AP computer science has likewise increased. AI has the potential to have a transformative impact on society. As such it has become increasingly important to monitor public attitudes toward AI. Better understanding trends in public opinion is essential in informing decisions pertaining to AI’s development, regulation, and use.

This chapter examines public opinion through global, national, demographic, and ethnic lenses. Moreover, we explore the opinions of AI researchers, and conclude with a look at the social media discussion that surrounded AI in 2022. We draw on data from two global surveys, one organized by IPSOS, and another by Lloyd’s Register Foundation and Gallup, along with a U.S-specific survey conducted by PEW Research.

It is worth noting that there is a paucity of longitudinal survey data related to AI asking the same questions of the same groups of people over extended periods of time. As AI becomes more and more ubiquitous, broader efforts at understanding AI public opinion will become increasingly important.

In a 2022 IPSOS survey, 78% of Chinese respondents (the highest proportion of surveyed countries) agreed with the statement that products and services using AI have more benefits than drawbacks. After Chinese respondents, those from Saudi Arabia (76%) and India (71%) felt the most positive about AI products. Only 35% of sampled Americans (among the lowest of surveyed countries) agreed that products and services using AI had more benefits than drawbacks.

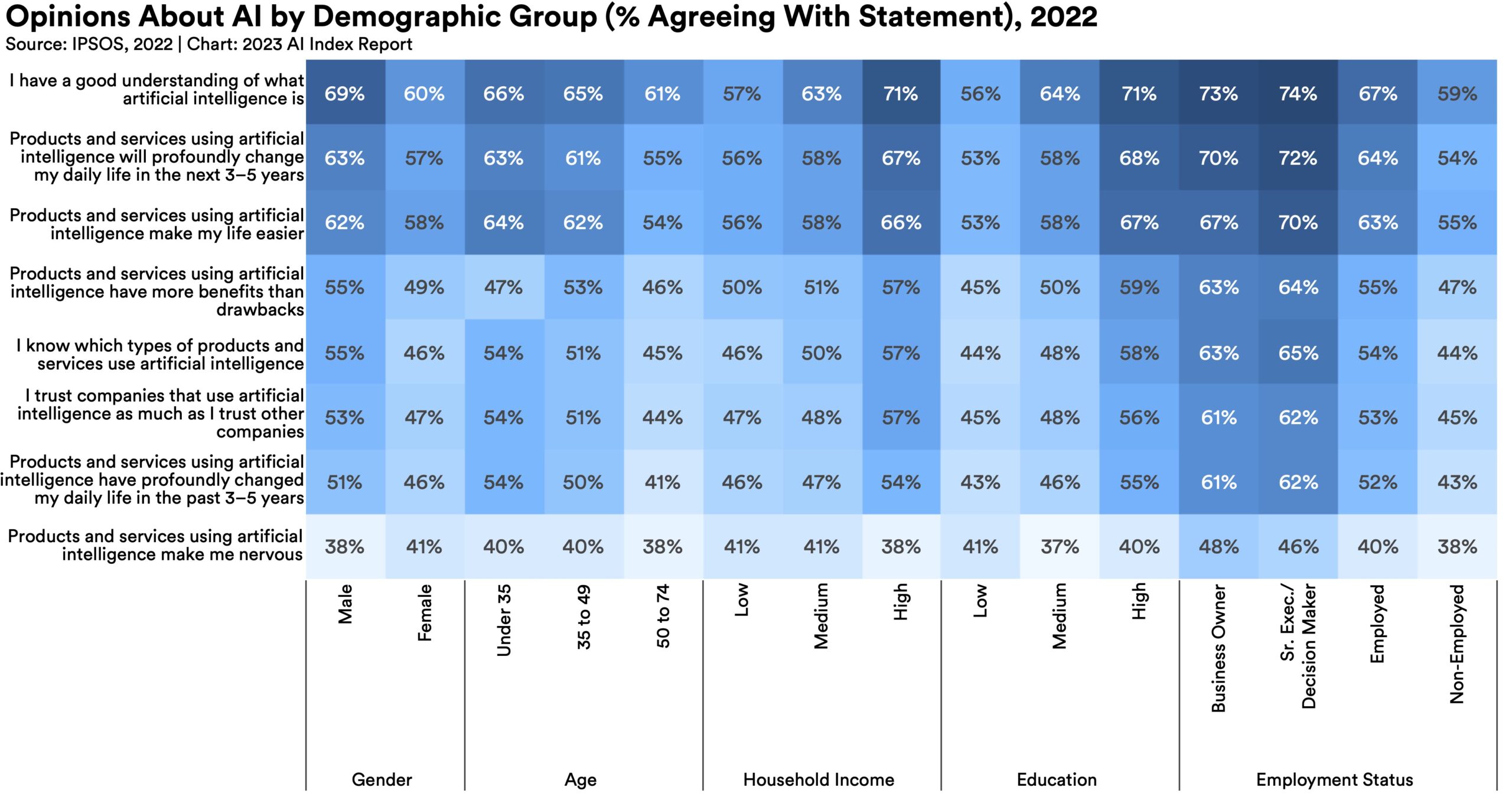

In a 2022 IPSOS survey, 78% of Chinese respondents (the highest proportion of surveyed countries) agreed with the statement that products and services using AI have more benefits than drawbacks. After Chinese respondents, those from Saudi Arabia (76%) and India (71%) felt the most positive about AI products. Only 35% of sampled Americans (among the lowest of surveyed countries) agreed that products and services using AI had more benefits than drawbacks.  According to the 2022 IPSOS survey, men are more likely than women to report that AI products and services make their lives easier, trust companies that use AI, and feel that AI products and services have more benefits than drawbacks. A 2021 survey by Gallup and Lloyd’s Register Foundation likewise revealed that men are more likely than women to agree with the statement that AI will mostly help rather than harm their country in the next 20 years.

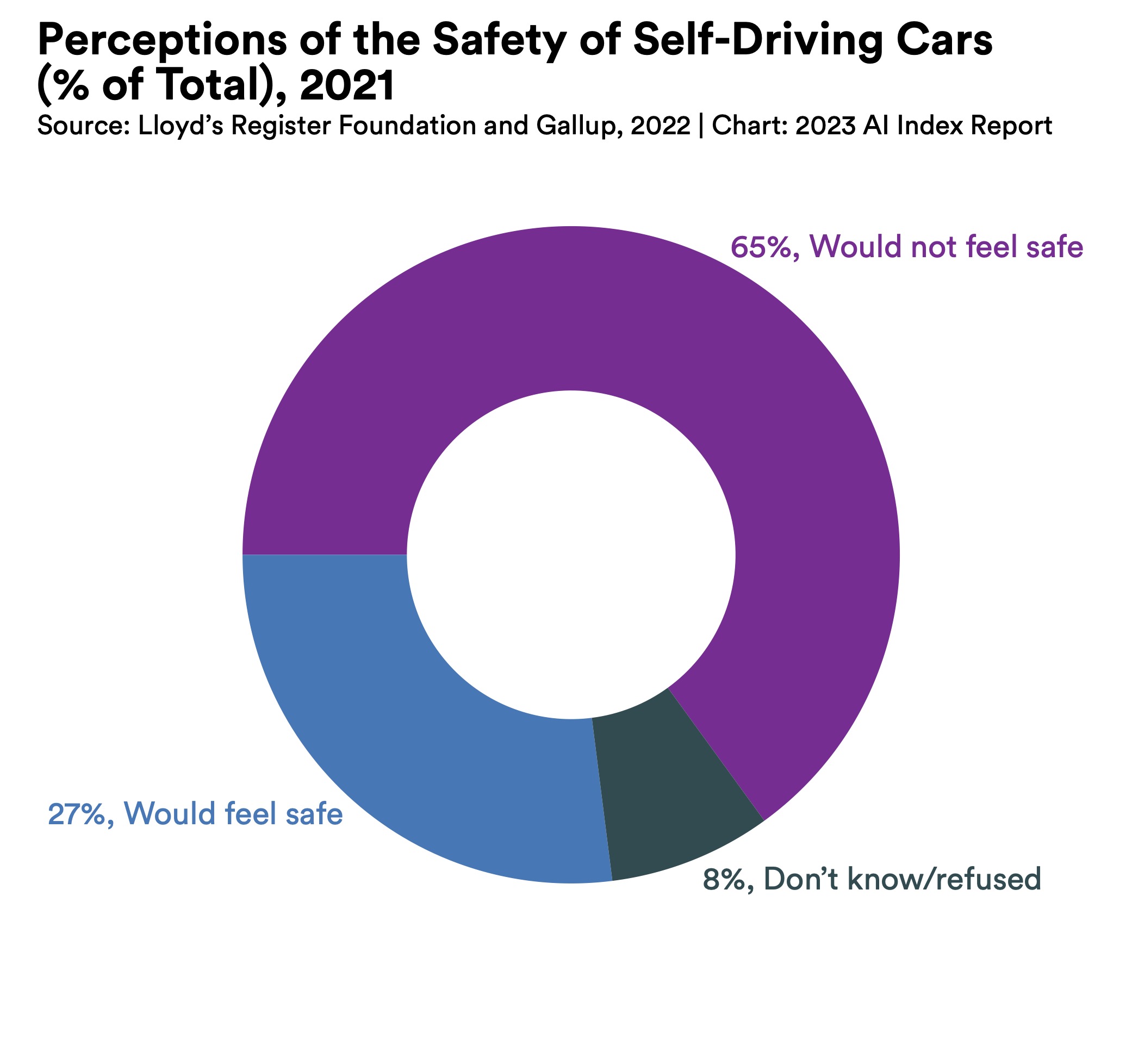

According to the 2022 IPSOS survey, men are more likely than women to report that AI products and services make their lives easier, trust companies that use AI, and feel that AI products and services have more benefits than drawbacks. A 2021 survey by Gallup and Lloyd’s Register Foundation likewise revealed that men are more likely than women to agree with the statement that AI will mostly help rather than harm their country in the next 20 years.  In a global survey, only 27% of respondents reported feeling safe in a self-driving car. Similarly, Pew Research suggests that only 26% of Americans feel that driverless passenger vehicles are a good idea for society.

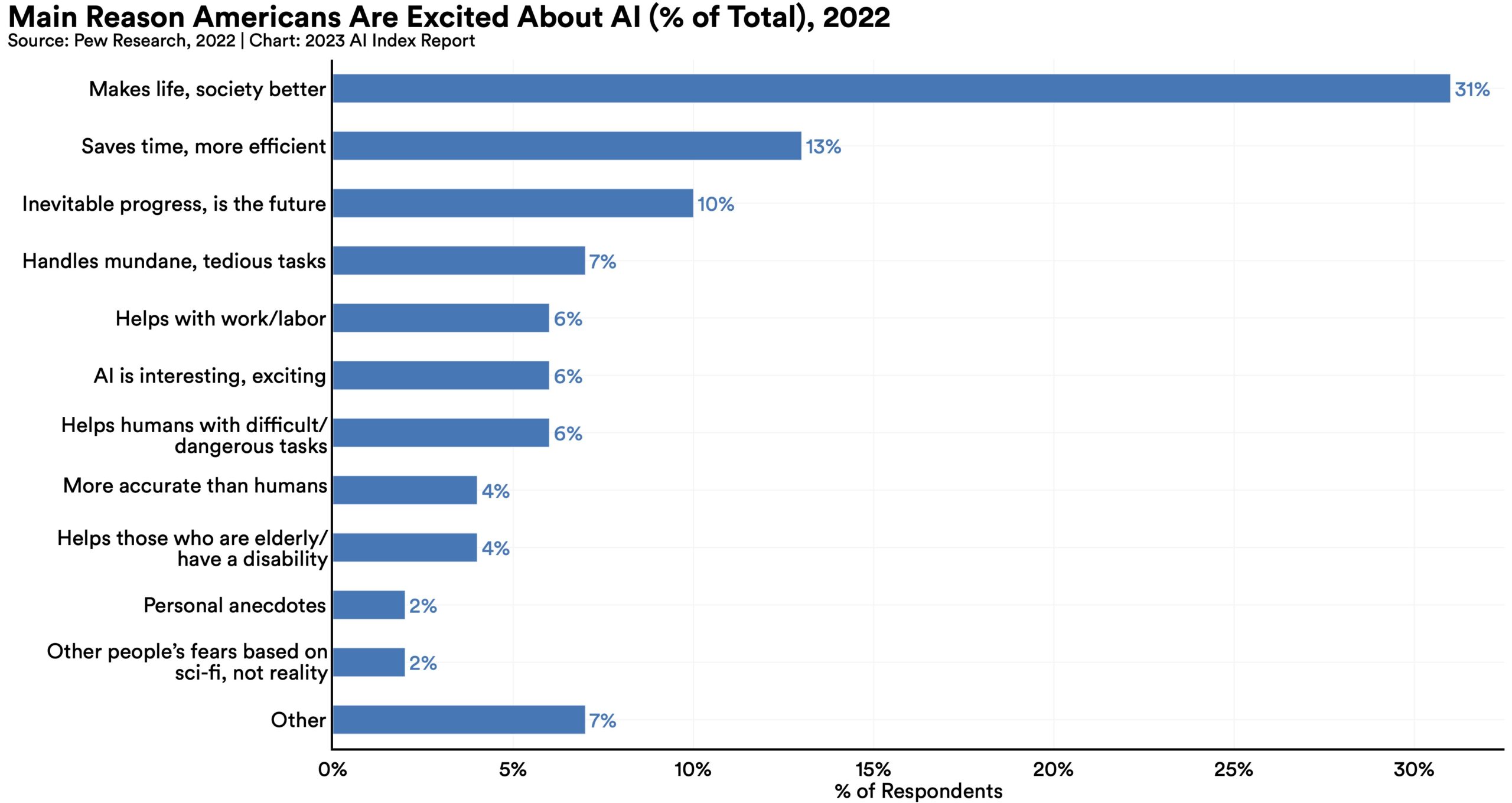

In a global survey, only 27% of respondents reported feeling safe in a self-driving car. Similarly, Pew Research suggests that only 26% of Americans feel that driverless passenger vehicles are a good idea for society.  Among a sample of surveyed Americans, those who report feeling excited about AI are most excited about the potential to make life and society better (31%) and to save time and make things more efficient (13%). Those who report feeling more concerned worry about the loss of human jobs (19%); surveillance, hacking, and digital privacy (16%); and the lack of human connection (12%).

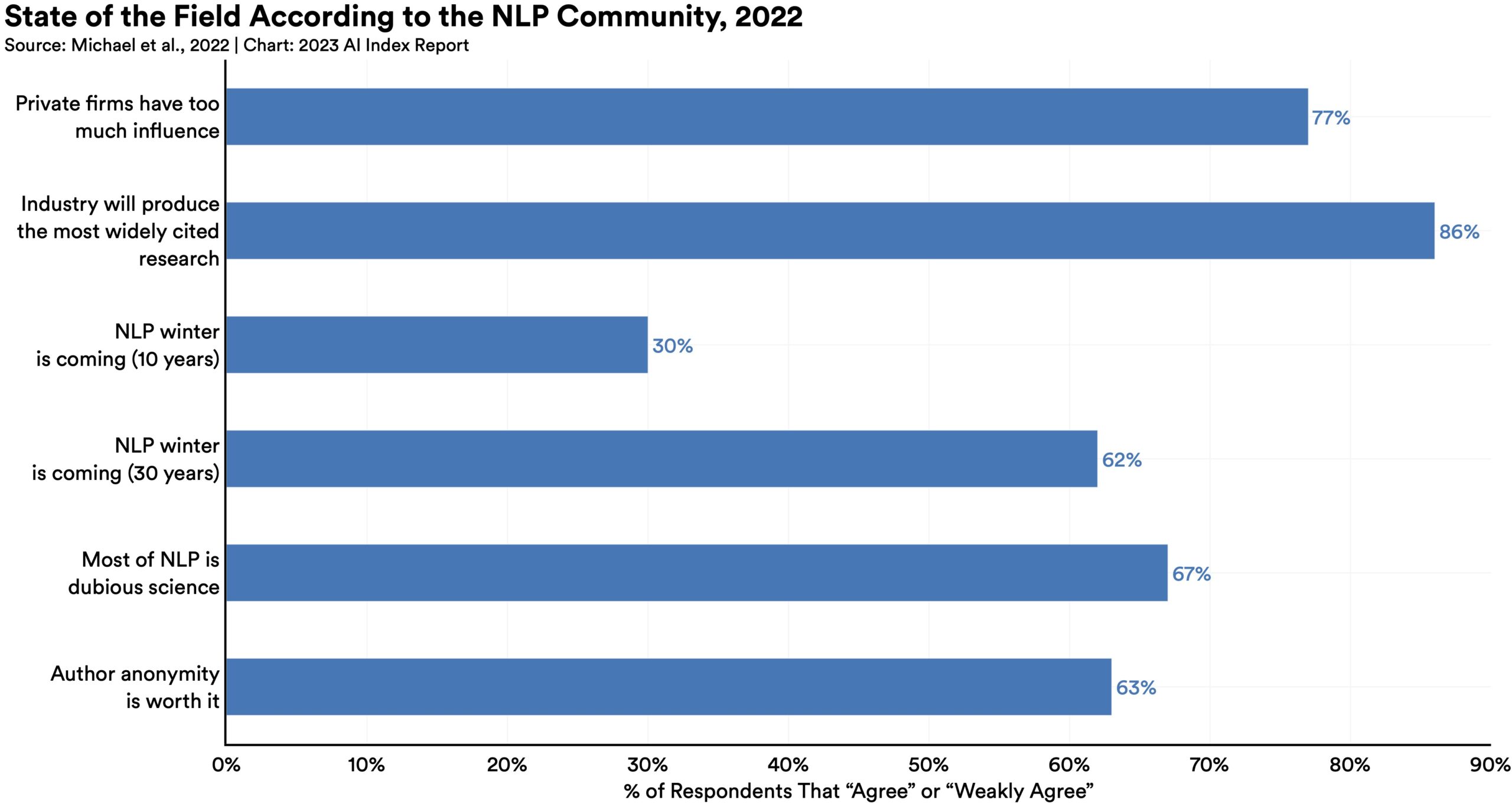

Among a sample of surveyed Americans, those who report feeling excited about AI are most excited about the potential to make life and society better (31%) and to save time and make things more efficient (13%). Those who report feeling more concerned worry about the loss of human jobs (19%); surveillance, hacking, and digital privacy (16%); and the lack of human connection (12%).  According to a survey widely distributed to NLP researchers, 77% either agreed or weakly agreed that private AI firms have too much influence, 41% said that NLP should be regulated, and 73% felt that AI could soon lead to revolutionary societal change. These were some of the many strong opinions held by the NLP research community.

According to a survey widely distributed to NLP researchers, 77% either agreed or weakly agreed that private AI firms have too much influence, 41% said that NLP should be regulated, and 73% felt that AI could soon lead to revolutionary societal change. These were some of the many strong opinions held by the NLP research community.